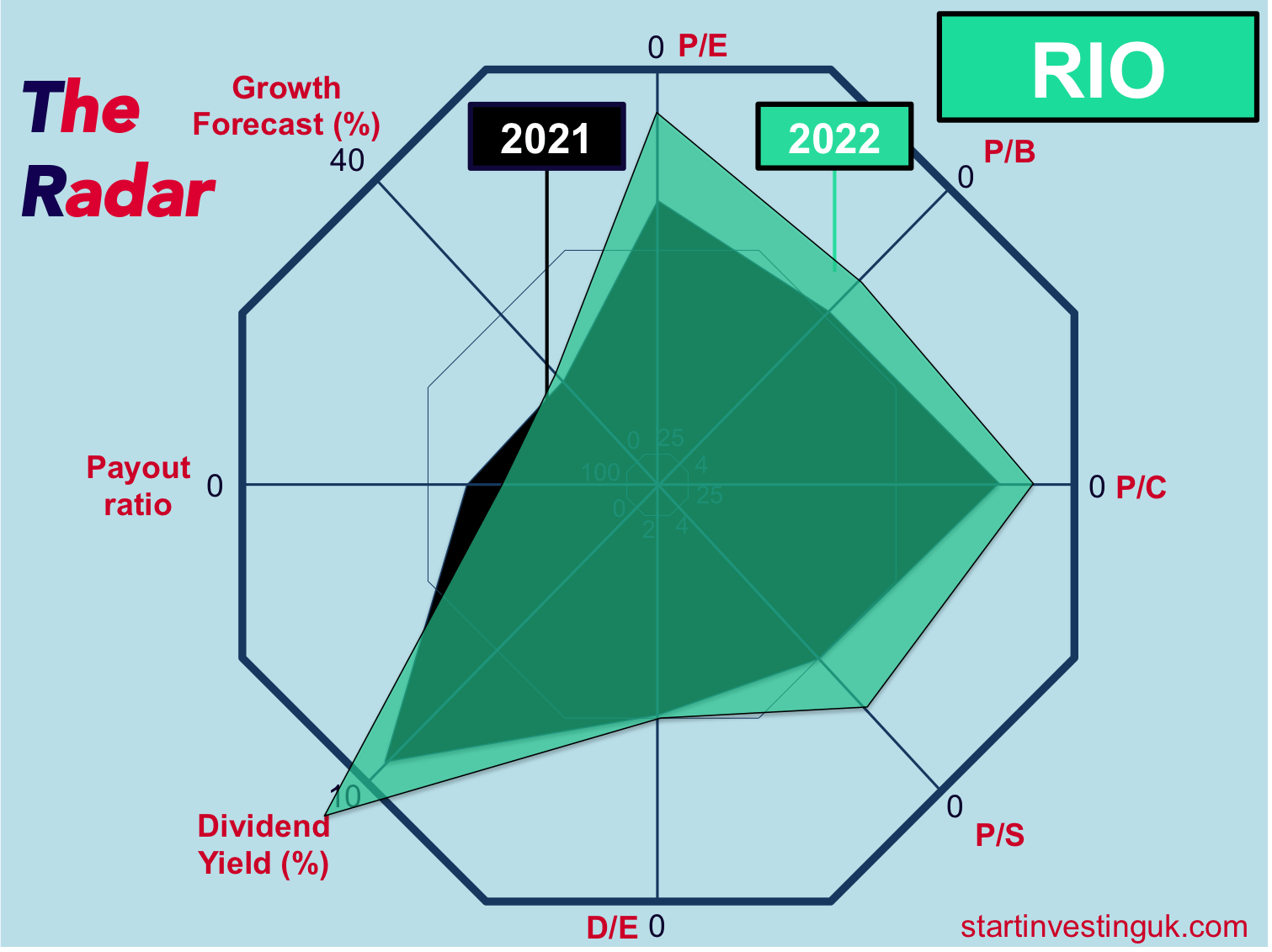

Why We Bought in 2021 - Strong financials

- Incredibly well-run, historic company

- Excellent business strategy

- Competitive advantage and a wide moat

- History of maintaining and increasing their dividend payments

Why we're reinvesting in 2022

All of the above is still

true, and now we can add that they have made an

enormous amount of cash in the last calendar year.

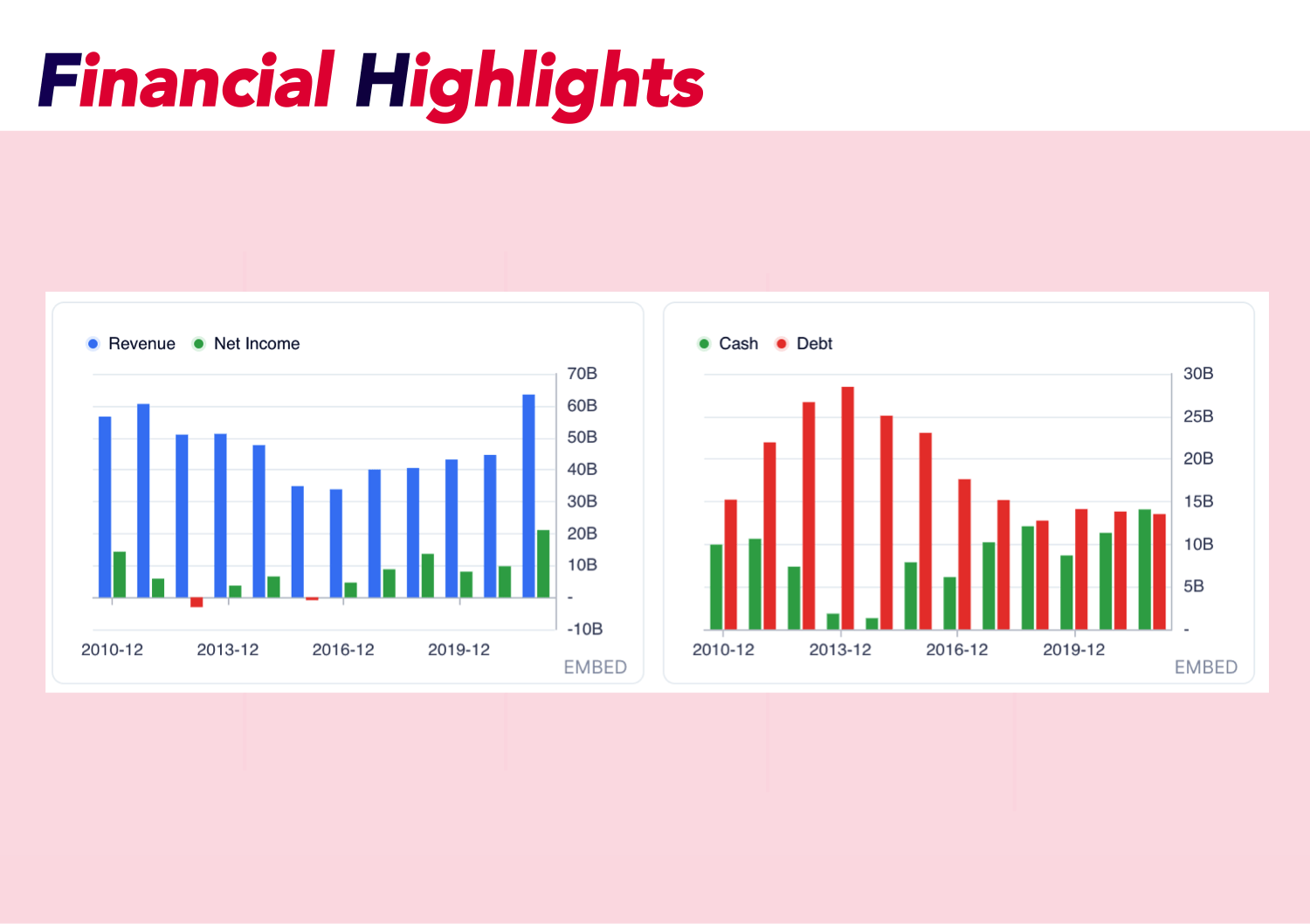

In February, Rio Tinto reported its year-end financials, which featured a company

record for cash flow. Whereas Rio Tinto generated free cash flow of

£8.4 billion in 2020, the company set a new high-water mark in 2021, reporting free cash flow of

£14.2 billion. The driving forces behind the

strong cash flow growth came from the aluminium and copper businesses, which accounted for year-over-year free cash flow growth of

155% and

289%, respectively.

Unsurprisingly, this ample cash flow growth has helped the company shore up its balance sheet. Rio Tinto's CEO, Jakob Stausholm, said the company's balance sheet is now "the

strongest it's been for at least 15 years," in the press release accompanying the earnings report. Rio Tinto ended 2021 with a net cash position of

£1.3 billion, representing a considerably more

robust position than where it was at the end of 2020.

If you look at the financials at the moment, it isn't hard to see why the CEO is happy with the current situation:

- Strong financials

- Incredibly well-run, historic company

- Excellent business strategy

- Competitive advantage and a wide moat

- History of maintaining and increasing their dividend payments

Why we're reinvesting in 2022

In February, Rio Tinto reported its year-end financials, which featured a company record for cash flow. Whereas Rio Tinto generated free cash flow of £8.4 billion in 2020, the company set a new high-water mark in 2021, reporting free cash flow of £14.2 billion. The driving forces behind the strong cash flow growth came from the aluminium and copper businesses, which accounted for year-over-year free cash flow growth of 155% and 289%, respectively.