Recap

This month we have decided to reinvest into KMR despite a 18% drop in its share price since our initial investment. Let's start with a recap of what the company is all about.

How do Kenmare PLC make money?Kenmare has established itself as a prominent player in the global industrial minerals market. Its core business revolves around the extraction and sale of titanium minerals, particularly ilmenite and rutile. Here's a closer look at how Kenmare Resources generates revenue and profits.

1. Mining Expertise:

Kenmare Resources' primary source of income is its flagship operation, the Moma Titanium Minerals Mine, located in Mozambique. The company's mining prowess allows it to extract valuable mineral sands efficiently. This expertise is vital to the company's bottom line, as it ensures a steady supply of raw materials for processing.

2. Mineral Processing: Once the mineral sands are extracted, Kenmare Resources employs advanced processing techniques to separate ilmenite and rutile from the ore. Ilmenite is used in the production of titanium dioxide, which finds application in paints, plastics, and cosmetics, among other industries. Rutile is crucial for manufacturing titanium metal and welding electrodes.

3. Global Distribution:

Kenmare Resources has established a robust global distribution network, ensuring that its products reach customers around the world. This broad reach allows the company to capitalize on the strong demand for titanium minerals in various sectors, including construction, aerospace, and automotive.

4. Diversified Product Portfolio:

In addition to ilmenite and rutile, the company also mines and sells zircon, another valuable industrial mineral. Zircon is used in ceramics, refractories, and the production of high-performance materials. This diversified product portfolio helps Kenmare Resources weather market fluctuations and enhances its revenue streams.

5. Sustainable Practices:

Kenmare Resources places a strong emphasis on environmental responsibility and sustainability in its operations. This commitment not only aligns with global environmental standards but also appeals to socially conscious investors and customers.

Why are we continuing to back the company?

Solid Performance Amid ChallengesDespite some production challenges in 2023 and the first quarter of 2024, Kenmare has demonstrated resilience and a capacity to meet its production targets.

Production Highlights: - Ilmenite Production: Increased marginally to 205,500 tonnes in Q1 2024 from 204,300 tonnes in Q1 2023.

- Primary Zircon Production: Experienced a temporary dip, but Kenmare anticipates recovery in subsequent quarters.

- Operational Excellence: Achieved zero Lost Time Injuries in the first quarter, reflecting strong safety and operational management.

Market Dynamics and Strong DemandKenmare is benefiting from a robust market for its products, particularly ilmenite, driven by a rebound in titanium pigment demand and continued growth in the titanium metal sector. Despite a slight dip in average selling prices in 2023, the demand outlook for 2024 is strong, with Kenmare maintaining a solid order book.

Key Market Insights: - Titanium Pigment Demand: Recovering strongly, especially in Europe and North America.

- Titanium Metal Sector: Sustained strong demand supports Kenmare’s market position.

- Zircon Market: Showing signs of recovery, with increasing demand from India countering weaker European markets.

- Kenmare’s ability to adapt to market conditions and capitalize on demand trends is a significant positive indicator for future performance.

Strategic Capital ProjectsKenmare is investing in its future with strategic capital projects aimed at enhancing long-term production capabilities. The company is preparing to transition Wet Concentrator Plant (WCP) A to the Nataka ore zone, which holds over 70% of Moma’s mineral resources. This move is essential for securing decades of production.

Investment Highlights: - New Dredges: Higher capacity dredges are being fabricated to replace the existing ones.

- Desliming Circuit: Under construction to improve slimes management at Nataka.

- Tailings Storage Facility: In progress to replace the current paddock system, ensuring environmental and operational efficiency.

- Despite the increased cost of these projects, the long-term benefits outweigh the expenses, providing a clear path to sustained production and profitability.

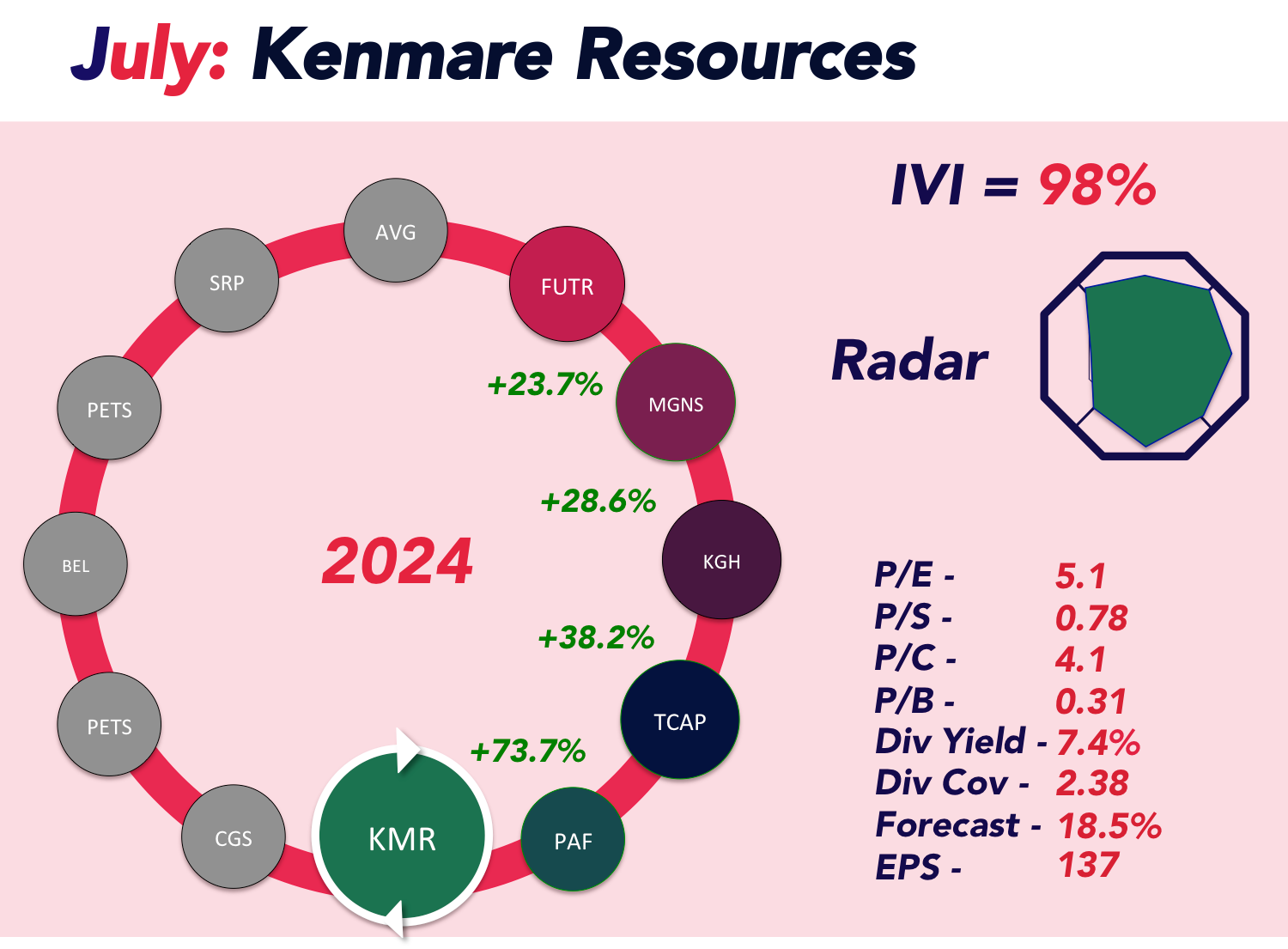

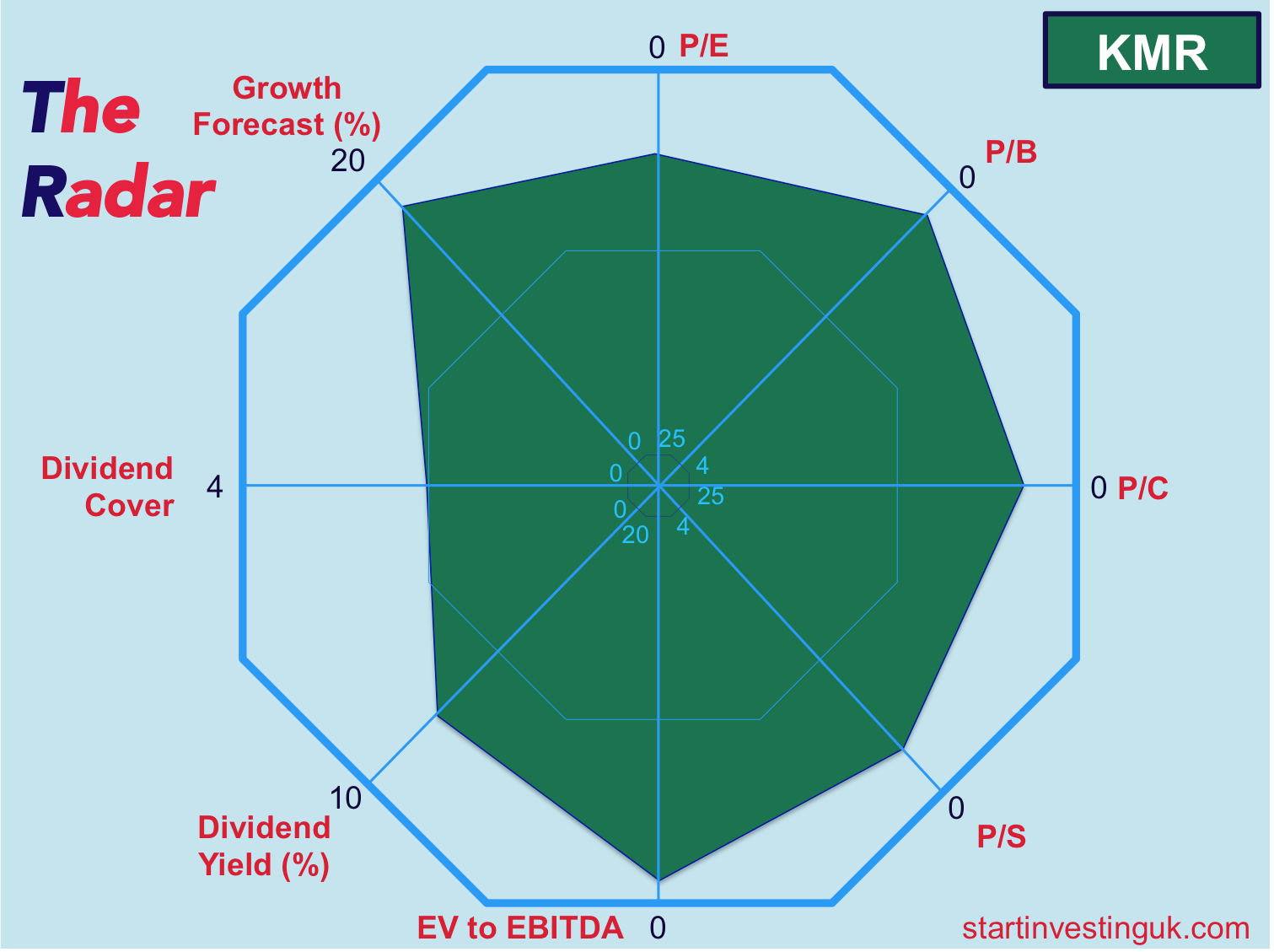

Financial Health and ValuationKenmare’s financial health is extremely robust, with strong earnings and a solid balance sheet. In 2023, the company reported cash profits of $220 million and increased its dividend by 3%, underscoring its commitment to returning value to shareholders. Despite these strengths, the market has undervalued Kenmare’s stock, presenting an attractive opportunity for investors.

Valuation Metrics: - Market Capitalization: £269 million, significantly lower than the $900 million value of its assets.

- Debt Management: New $200 million loan secured to support capital projects, with a manageable debt load.

- Analysts, including those from Peel Hunt, believe that the current stock price does not fully reflect Kenmare’s potential, especially given the sustained ilmenite pricing and the unlocking of long-term value through its investment programs.

Looking AheadKenmare is on track to achieve its 2024 production guidance, with expectations of improved performance in the coming quarters. The company’s strategic initiatives, coupled with favorable market conditions, position it well for future growth.

ConclusionWe believe Kenmare Resources stands out as a hidden gem in the mining industry. Its operational excellence, strategic investments, and strong market demand create a robust foundation for future growth. With the stock currently undervalued, we will be adding to our investment on Monday.

- Ilmenite Production: Increased marginally to 205,500 tonnes in Q1 2024 from 204,300 tonnes in Q1 2023.

- Primary Zircon Production: Experienced a temporary dip, but Kenmare anticipates recovery in subsequent quarters.

- Operational Excellence: Achieved zero Lost Time Injuries in the first quarter, reflecting strong safety and operational management.

- Titanium Pigment Demand: Recovering strongly, especially in Europe and North America.

- Titanium Metal Sector: Sustained strong demand supports Kenmare’s market position.

- Zircon Market: Showing signs of recovery, with increasing demand from India countering weaker European markets.

- Kenmare’s ability to adapt to market conditions and capitalize on demand trends is a significant positive indicator for future performance.

- New Dredges: Higher capacity dredges are being fabricated to replace the existing ones.

- Desliming Circuit: Under construction to improve slimes management at Nataka.

- Tailings Storage Facility: In progress to replace the current paddock system, ensuring environmental and operational efficiency.

- Despite the increased cost of these projects, the long-term benefits outweigh the expenses, providing a clear path to sustained production and profitability.

- Market Capitalization: £269 million, significantly lower than the $900 million value of its assets.

- Debt Management: New $200 million loan secured to support capital projects, with a manageable debt load.

- Analysts, including those from Peel Hunt, believe that the current stock price does not fully reflect Kenmare’s potential, especially given the sustained ilmenite pricing and the unlocking of long-term value through its investment programs.