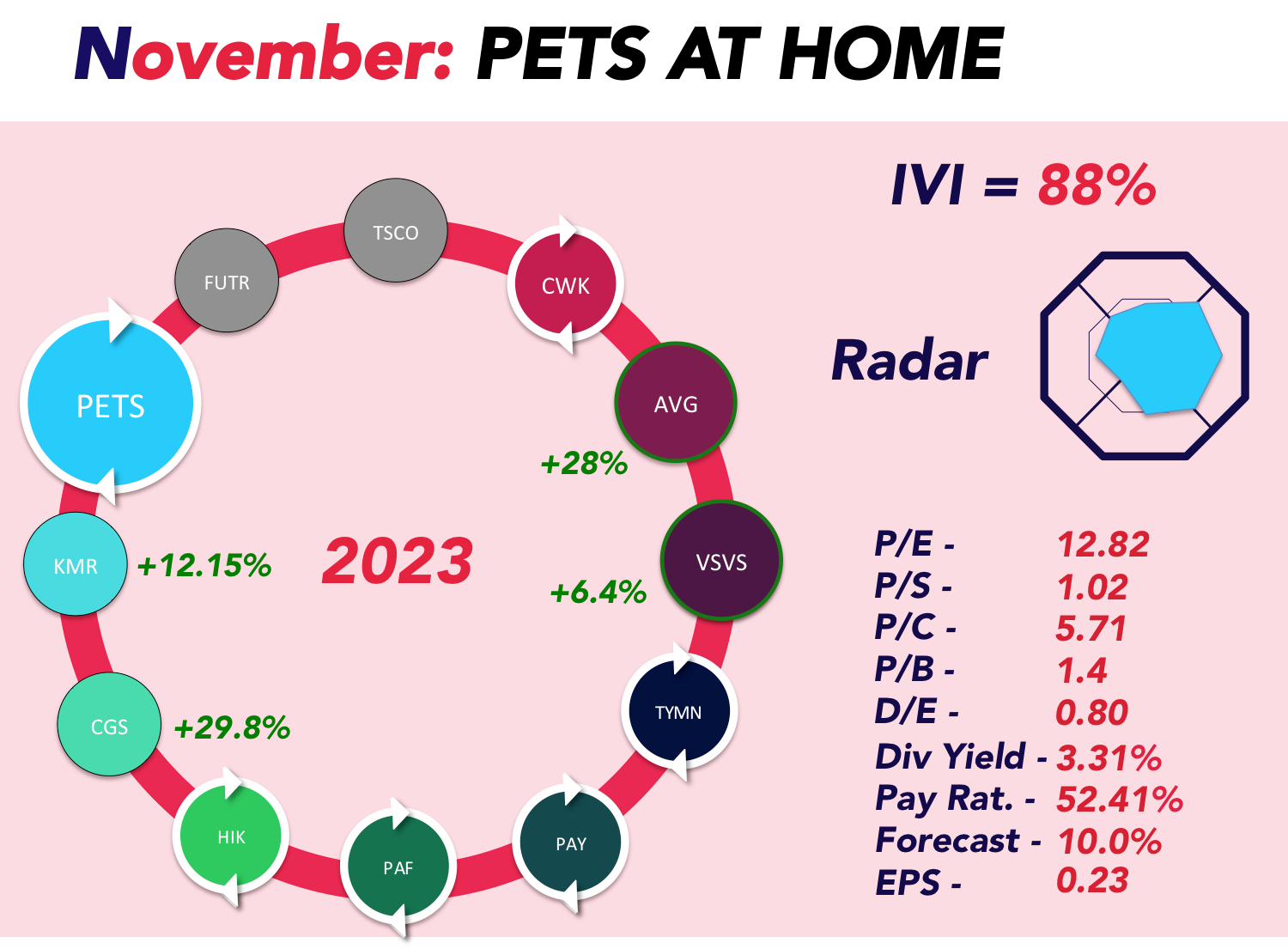

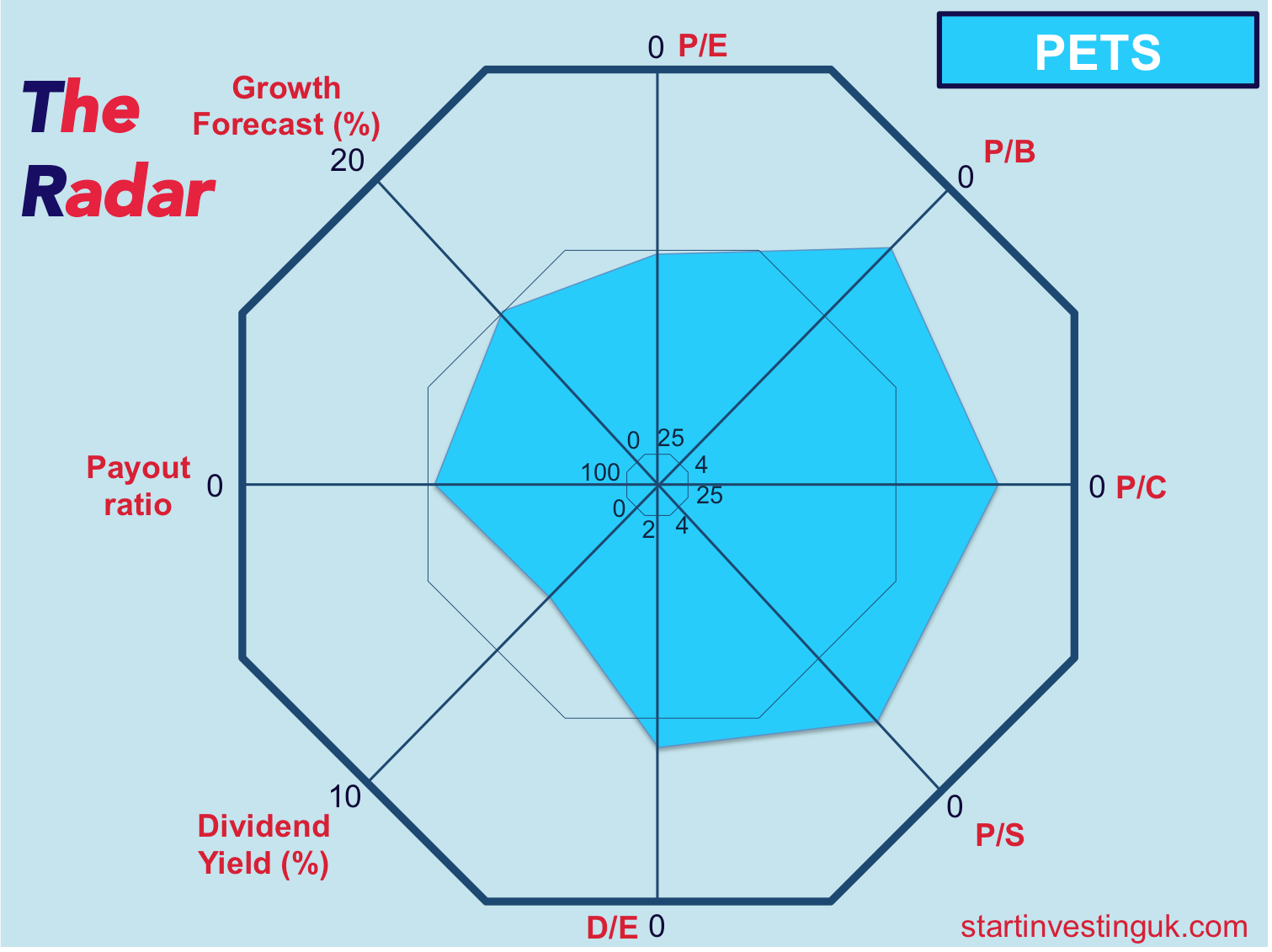

Price drop for PETS presents an investment opportunity

Pets at Home (PETS) recently experienced a 21% decline in its share price, falling to around 300p, following the launch of a

Competition and Markets Authority (CMA) review into the UK's veterinary services market, valued at over £2 billion. This inquiry was initiated due to concerns about potential anti-competitive practices that might be impacting pet owners' access to fair and transparent information on treatment options and pricing.

While this regulatory scrutiny has hit both Pets at Home and other veterinary groups in the UK, the dip in Pets at Home's share price presents an intriguing opportunity for investors eyeing the long-term growth prospects of this prominent player in the pet care industry.

Market Analysis and Potential Impact on Pets at Home:

The rising trend in pet ownership, particularly after the pandemic-induced surge in demand for puppies and kittens, has seen pets become integral members of families. In times of urgent medical care needs for these beloved companions, pet owners might not extensively compare prices for such services, unlike other consumer sectors.

This has been evident by their Q1 FY24 Trading Statement for the 16 week period to 20 July 2023, which was released in August. Highlights of the statement included: - Consumer revenue up 10.2% to £568.2m supported by both volume and value growth.

- Consumer numbers continued to grow with our active VIP base increasing 4% to 7.7m, with over 22,000 new Puppy & Kitten sign ups and 18,000 new pet registrations a week in our Vet Group.

- Total Group revenue growth of 7.9% to £436.8m, with Group like-for-like (LFL) revenue up 7.9%.

- Vet Group revenue was up 16.3%, with LFL2 of 16.6%, increasingly supported by number of visits (as we increased vet capacity), improving mix and continued growth in average spend.

- Retail revenue growth of 7.1%, and LFL2 up 7.1%.

- Food category remains in volume growth across grocery and premium categories supported by further progress in our relative price position.

- Accessories trends were consistent with previous quarters, as expected.

The CMA aims to ensure that pet owners receive value for their money amid economic strains. Their concern over the apparent increase in the cost of veterinary services, surpassing the inflation rate, signals the need for a comprehensive evaluation of this industry. Pets at Home's business model encompasses a small animal veterinary segment in addition to its primary focus on retail, offering an array of pet products through its numerous stores across the UK.

The CMA review's potential impact on Pets at Home remains a point of concern for investors. Nonetheless, Pets at Home's core revenue stream stems from retail sales, spanning from pet food to accessories, across its extensive network of 458 stores. The company's diversified approach, with veterinary services forming a smaller part of its revenue model, might offer a more resilient stance amid regulatory uncertainties compared to other veterinary groups.

Response and Future Outlook:

In response to the CMA's inquiry, the profession has emphasized its commitment to fair pricing aligned with the value it provides. The companies have pointed out the significant shortage of vets in the UK, contributing to cost pressures, and highlighted that their pricing structures aim to accommodate these challenges.

Investment Perspective:

Despite the temporary setback witnessed in share prices due to the CMA review, Pets at Home presents an intriguing investment opportunity. The company's focus on retail as its primary revenue driver, coupled with its position as a leading player in the pet care industry, provides a relatively stable footing amidst market uncertainties. The recent decline in share price could potentially offer a chance for us to acquire Pets at Home shares at a low valuation.

- Consumer revenue up 10.2% to £568.2m supported by both volume and value growth.

- Consumer numbers continued to grow with our active VIP base increasing 4% to 7.7m, with over 22,000 new Puppy & Kitten sign ups and 18,000 new pet registrations a week in our Vet Group.

- Total Group revenue growth of 7.9% to £436.8m, with Group like-for-like (LFL) revenue up 7.9%.

- Vet Group revenue was up 16.3%, with LFL2 of 16.6%, increasingly supported by number of visits (as we increased vet capacity), improving mix and continued growth in average spend.

- Retail revenue growth of 7.1%, and LFL2 up 7.1%.

- Food category remains in volume growth across grocery and premium categories supported by further progress in our relative price position.

- Accessories trends were consistent with previous quarters, as expected.

Conclusion

While the ongoing CMA review poses some short-term uncertainties for both Pets at Home and CVS, the fundamental growth prospects of Pets at Home, driven by the booming pet care market, remain robust. Investors considering a long-term perspective might view the current share price drop as an opportunity to potentially acquire a stake in a company with a solid foothold in the pet care sector, despite short-term regulatory challenges.

Conclusion