Overview

Tyman plc is a

leading supplier of engineered components to the door and window industry. The company operates in three business units: AmesburyTruth, ERA, and Schlegel International.

The housing market has gone through some

turbulent times since we invested in April 2022. However, Tyman has retained a strong financial position, a healthy balance sheet and continues to produce solid returns despite a

challenging climate. The liklihood is that the short term will be a little

rocky for the housing market, and possibly we may see a further

decline in share price in the

short term. However, based on our metrics, Tyman is more

undervalued now than when we last bought in, and has some

attributes which make it a good long term investment.

Tyman's business model is

well-diversified across regions and products; the company operates in various geographies and serves a

broad range of customer segments, providing a

varied product portfolio that caters to the needs of

many different end markets.

The business has shown its commitment to

sustainability and reducing its environmental impact, setting

ambitious targets to reduce its carbon footprint and increase the use of

sustainable materials in its products. We believe this focus on sustainability will help Tyman plc meet the

evolving needs of customers who are increasingly demanding environmentally responsible products.

The company also has a

strong track record of innovation and

quality, positioning it well to capture

growth opportunities in the door and window industry. The increasing demand for energy-efficient homes and buildings is driving the

demand for high-performance doors and windows, and Tyman plc's products are well-suited to meet these demands.

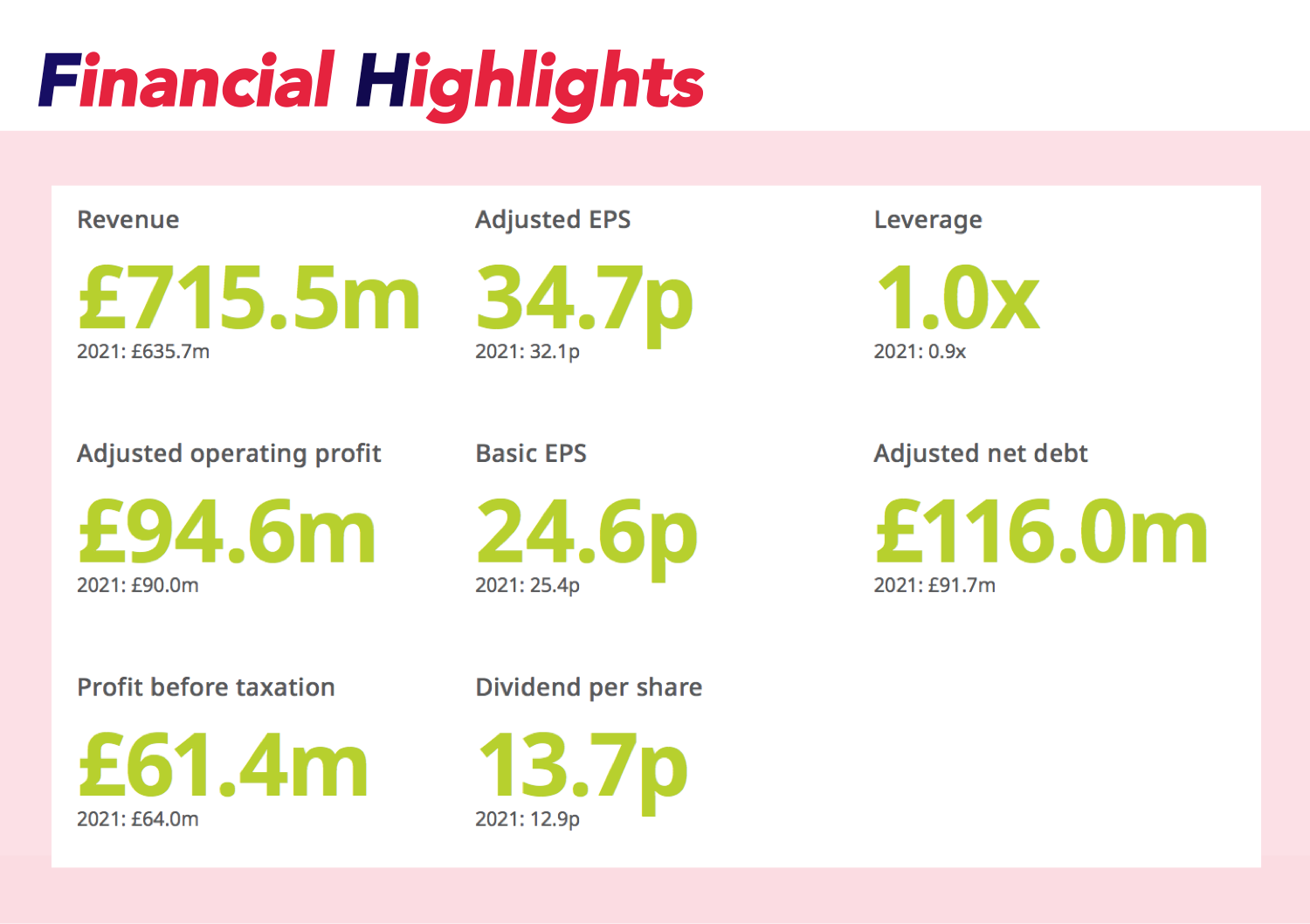

- Revenue growth of

13%, with like-for-like (LFL) growth of

5% reflecting successful pricing actions and share gains, partially offset by lower market volumes, including losses from exiting the Russian market

- Adjusted operating profit growth of

5%

- Full-year dividend increase of

6%.

Jo Hallas, Chief Executive Officer, commented: "The Group delivered a solid trading performance in 2022 against increasingly challenging market conditions. Our continued focus on share gains and improving our operational platform, together with successful implementation of pricing actions and strong cost control, enabled us to deliver full year adjusted operating profit at the upper end of market expectations.

We made further progress on our sustainability roadmap and the issuance of new sustainability-linked financing bolsters the Group's commitments to a more sustainable world. Pleasingly, this progress has been recognised by external agencies, most recently with Tyman's inclusion in the FTSE4Good UK Index.

In 2023, pricing carryover, self-help measures and benefits from strategic initiatives are expected to partially mitigate lower volumes and ongoing cost inflation as we navigate the near-term economic challenges. The underlying fundamentals of the markets the Group operates in remain strong. Building on our portfolio of differentiated products, market-leading brands, deep customer relationships and sustainability credentials, together with our agile and resilient business model, Tyman is well positioned to take advantage of the positive structural industry growth drivers as housing market conditions improve."

Reading between the lines here, TYMN are

streamlining their business and expect a

difficult short-term period. We are buying while market sentiment is

against them and will be holding for the medium term, collecting

dividends, and will be selling when times are good. Patience is an investor's friend - and this company isn't going anywhere.

- Revenue growth of 13%, with like-for-like (LFL) growth of 5% reflecting successful pricing actions and share gains, partially offset by lower market volumes, including losses from exiting the Russian market

- Adjusted operating profit growth of 5%

- Full-year dividend increase of 6%.

Conclusion

Based on Tyman's most recent financial report, the company has delivered a

solid trading performance in 2022 despite increasingly

challenging market conditions. The company has made progress on their sustainability roadmap, and their external recognition has

boosted their commitment to a more sustainable world. While they expect difficult short-term periods, they are well-positioned to take

advantage of

positive structural industry growth drivers in the

medium term. We are reinvesting in the company while market sentiment is

against them, collecting our

6% dividend, and holding for

better times ahead.

Conclusion