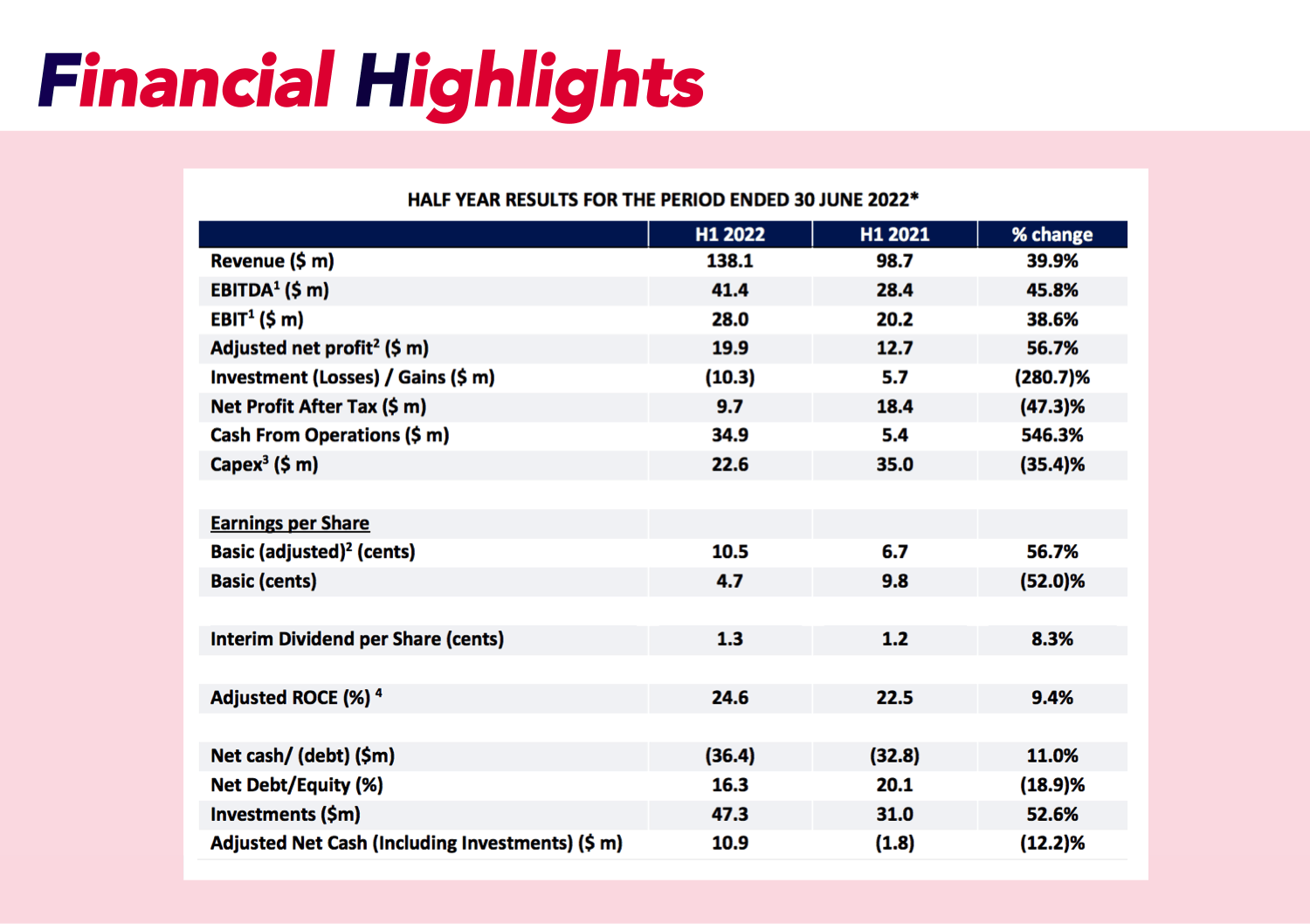

If you look closely at the results, Capital actually reported a

decrease in interim profit, but remarked that conditions "remain buoyant" and so

raised their full-year revenue outlook. Pretax profit in the six months to June 30 fell to

$15.1 million from

$24.3 million a year ago, despite revenue increasing

40% to

$138.1 million from

$98.7 million.

The company increased its revenue guidance for 2022 to between

$280-290 million from $270-280 million previously - great news for investors.

"Tendering activity across all business units remains robust, with a number of opportunities progressing," the Chair explained, "the underlying demand in the market continues to be

encouraging, as is evident from the high utilisation rates the group delivered in the first half. While there will be some seasonal slowdown through the third quarter, the tender pipeline remains

buoyant across drilling, mining and laboratories."

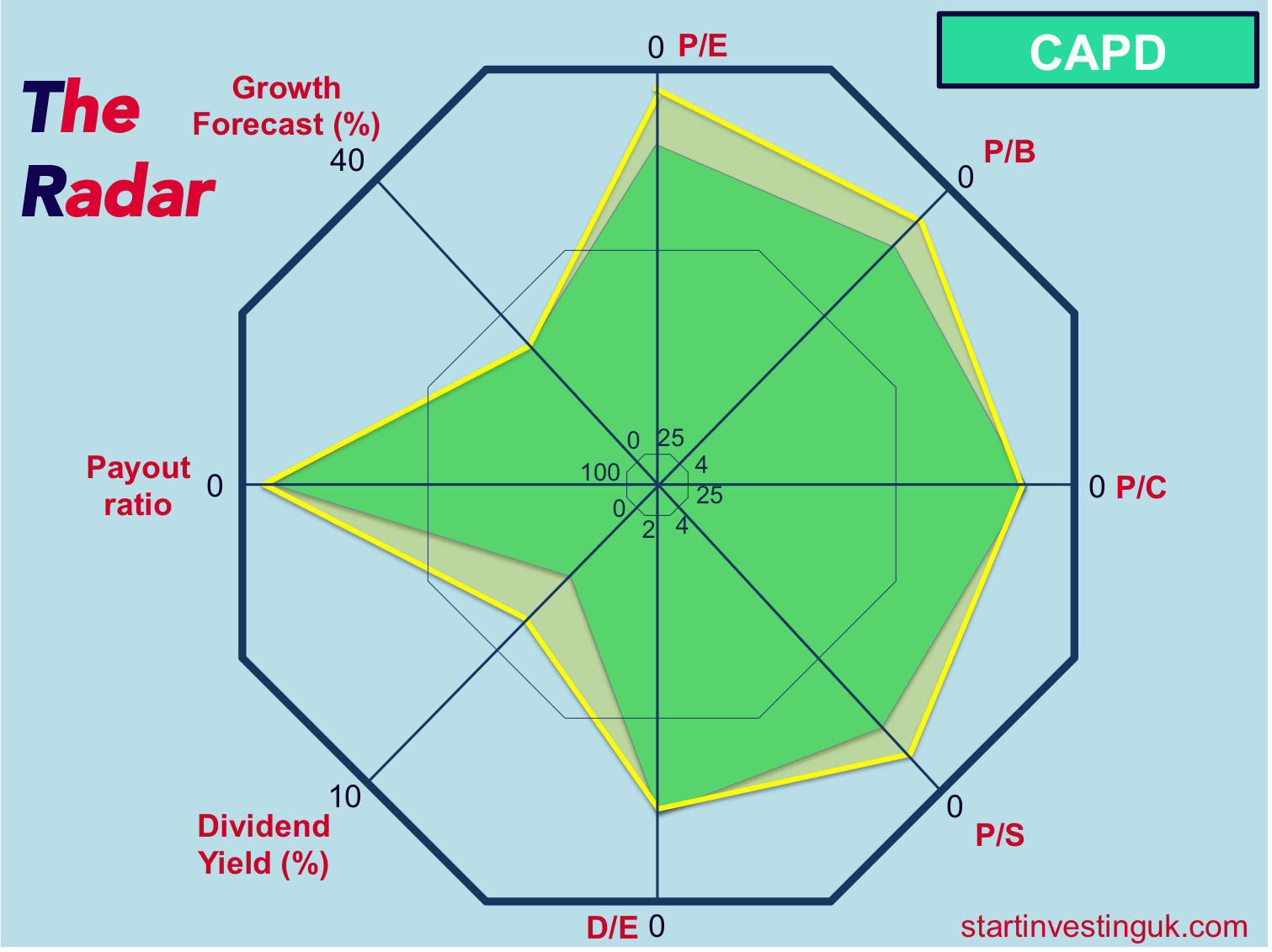

On top of this, CAPD have also

raised their dividend yield, now at 3.9%.

Conclusion

Despite an increase in

CAPD's share price since we last bought in, the company continues to go from

strength to

strength. With another

fantastic year on the cards in 2022 and a

dip in share price in recent weeks, we now feel that CAPD are once again

undervalued.

We will be

adding to our position in CAPD when the market opens tomorrow.