The top 10 stocks on our screen this month comprised either of companies

already added to the

CC portfolio, companies with

limited financial information, companies with

red flags (such as increasing debt) or companies with

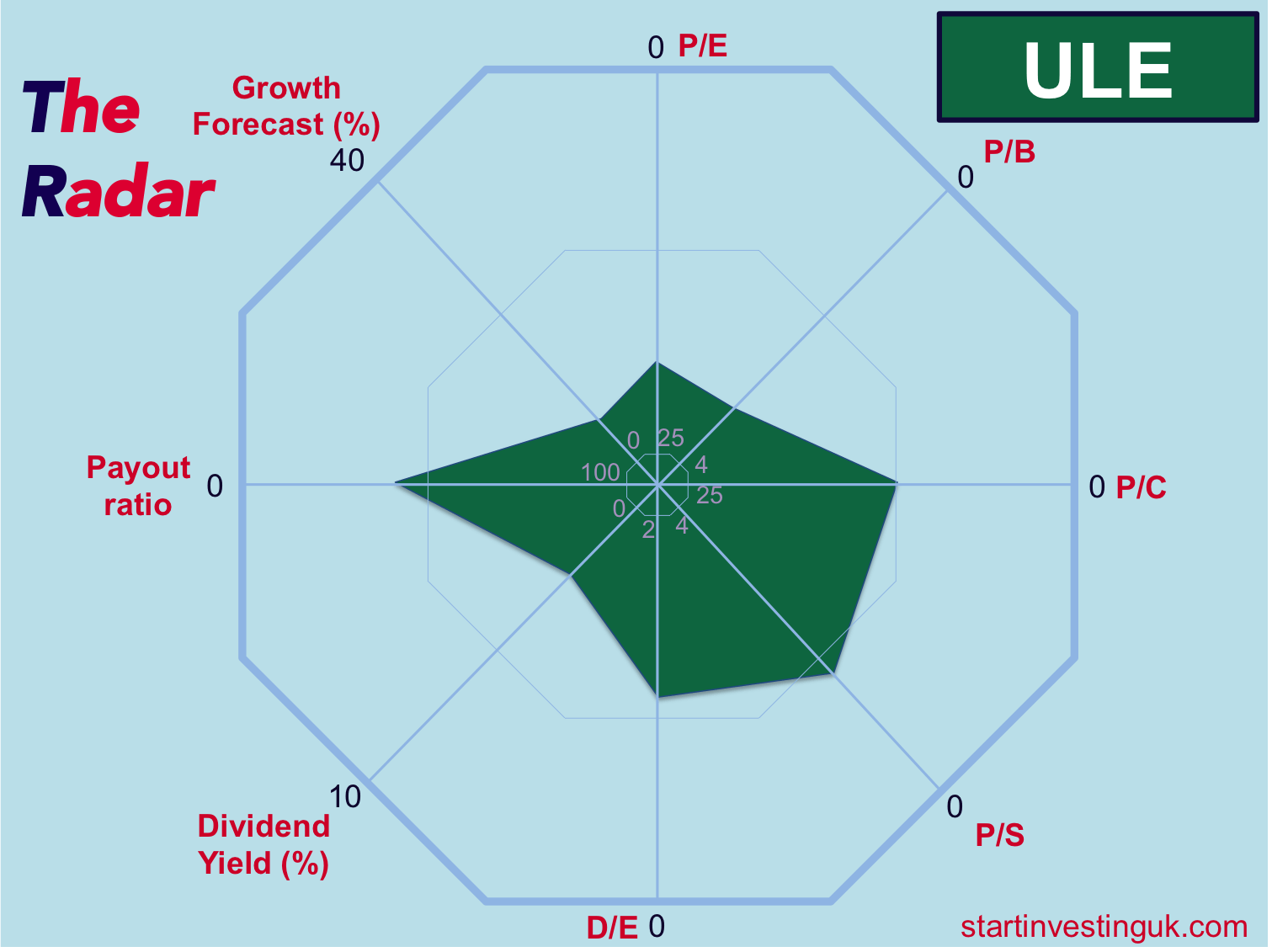

questionable ethics. So we have searched a little further afield on our list this month and have come across what appears to be a classic 'heads I win, tails I don't lose too much' pick. It is not a traditional value stock pick, as you will be able to see from the RADAR plot and it's financials. Though not currently undervalued, this pick is based on the

stability of the company's current outlook, with a possibility of a large amount of

growth if certain factors are in their favour.

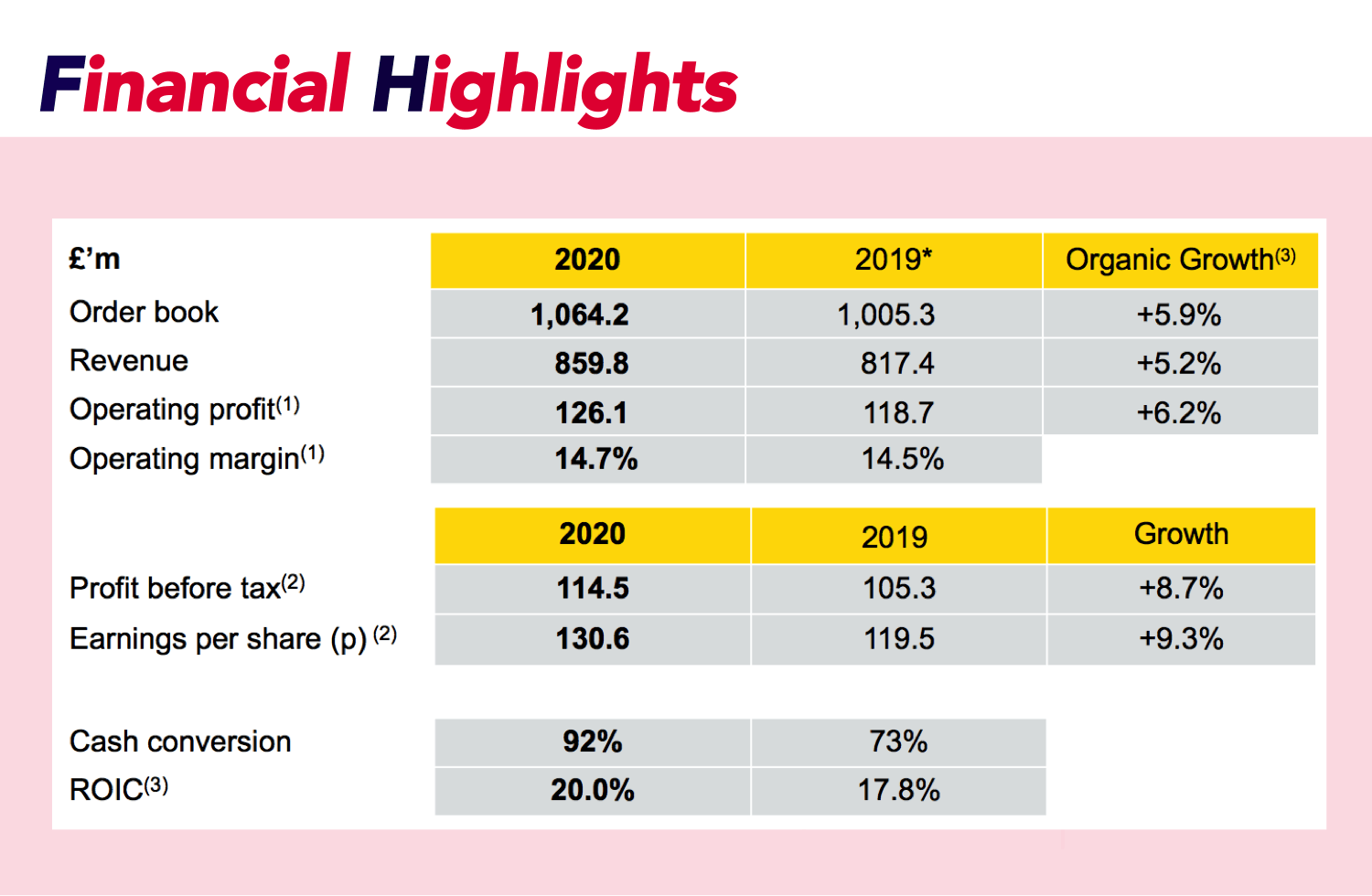

ULE had a

robust

performance in 2020, despite headwinds caused by COVID.

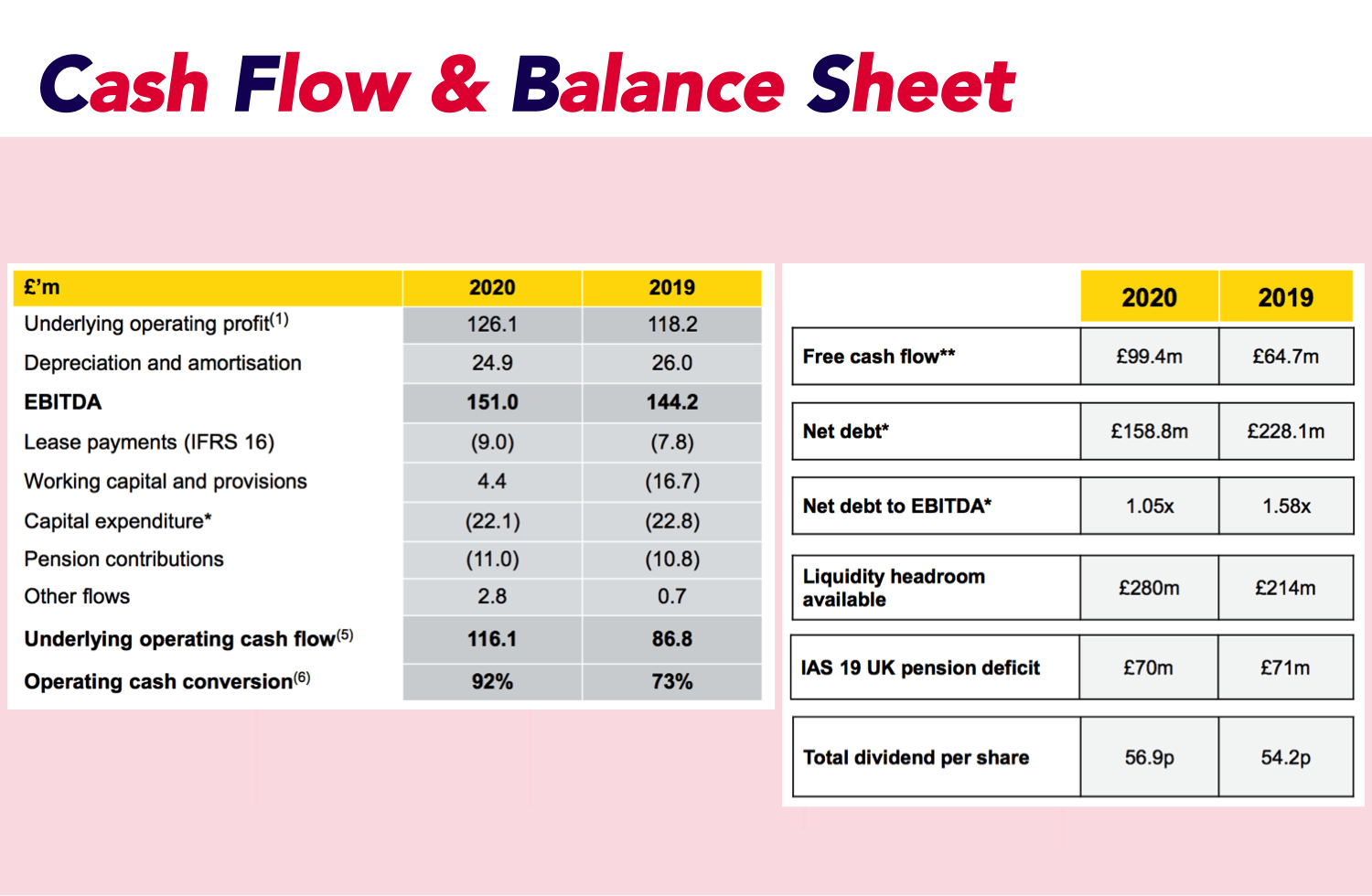

Single digit growth was seen in their order book, revenue, operating profit, profit before tax and earnings per share. They have also managed to pay down a significant portion of debt (£228.1m to £158.8m ) and

increase their free cash flow (£99.4m to £64.7m).

Some financial highlights are below, for more detail you can view their

annual report here:

Images courtesy of Ultra Electronics Holdings PLC.

How do

Ultra Electronics Holdings PLC

make their money?

- ULE provides electronic and software technologies for the defence, aerospace, security, transport, and energy markets.

- The company develops relationships with customers to

identify needs and

customise solutions. It has a wide product portfolio to sell differentiated technologies and systems for improving communication platforms.

- Thousands

of contracts are created with a multitude of customers each year.

- It reports in three segments:

- Maritime

- Intelligence and Communications

- Critical Detection and Control

- Approximately half of the revenue is derived from

North America and around one-third comes from the

United Kingdom.

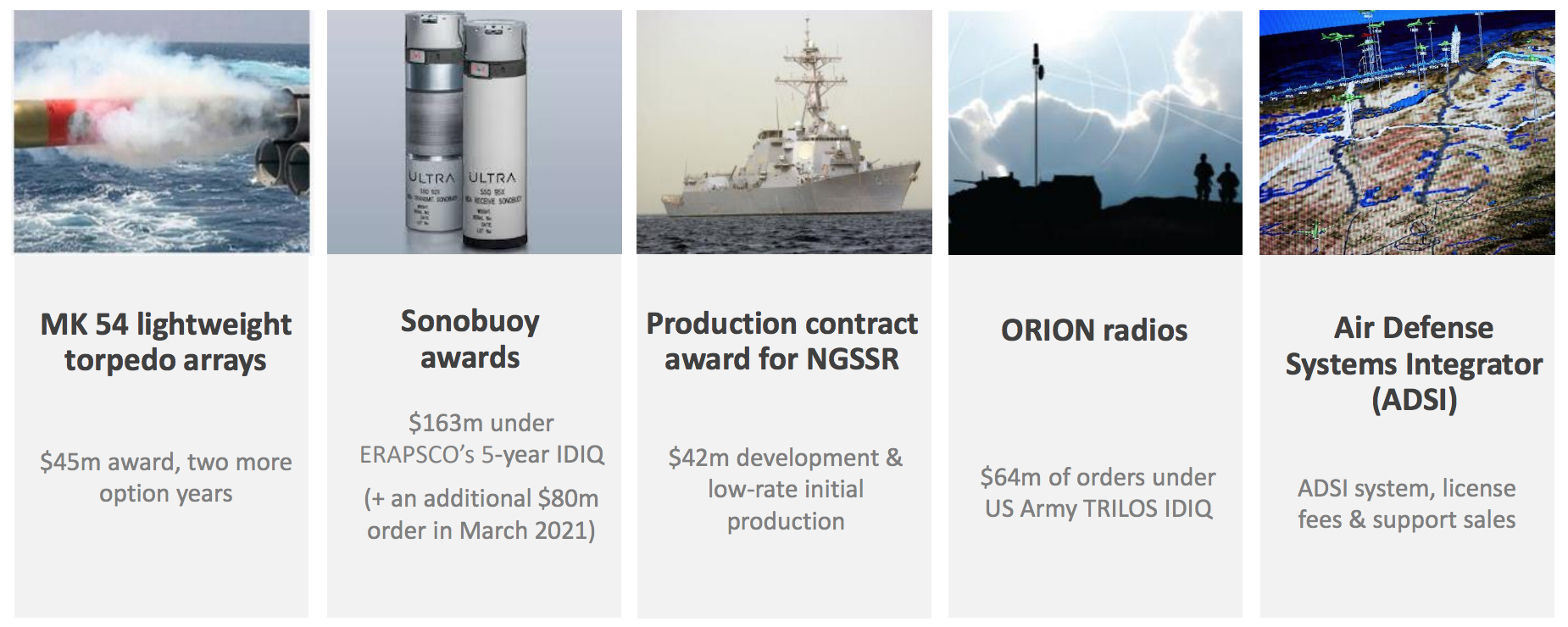

- If you are still thinking, 'yeah but what do they actually make?!' - here are a few

examples of the recent contracts that they have been awarded:

- ULE provides electronic and software technologies for the defence, aerospace, security, transport, and energy markets.

- The company develops relationships with customers to identify needs and customise solutions. It has a wide product portfolio to sell differentiated technologies and systems for improving communication platforms.

- Thousands of contracts are created with a multitude of customers each year.

- It reports in three segments:

- Maritime

- Intelligence and Communications

- Critical Detection and Control

- Approximately half of the revenue is derived from North America and around one-third comes from the United Kingdom.

- If you are still thinking, 'yeah but what do they actually make?!' - here are a few examples of the recent contracts that they have been awarded: