We are sure it will come as no surprise to learn that Kingfisher, the

second largest

home improvement retailer in Europe, has performed

very strongly

over the last

18 months. People have been trapped inside their homes, working from their homes and trying to sell their homes, meaning home improvement projects have

skyrocketed. Additionally, key Kingfisher stores such as

B&Q

and

Screwfix

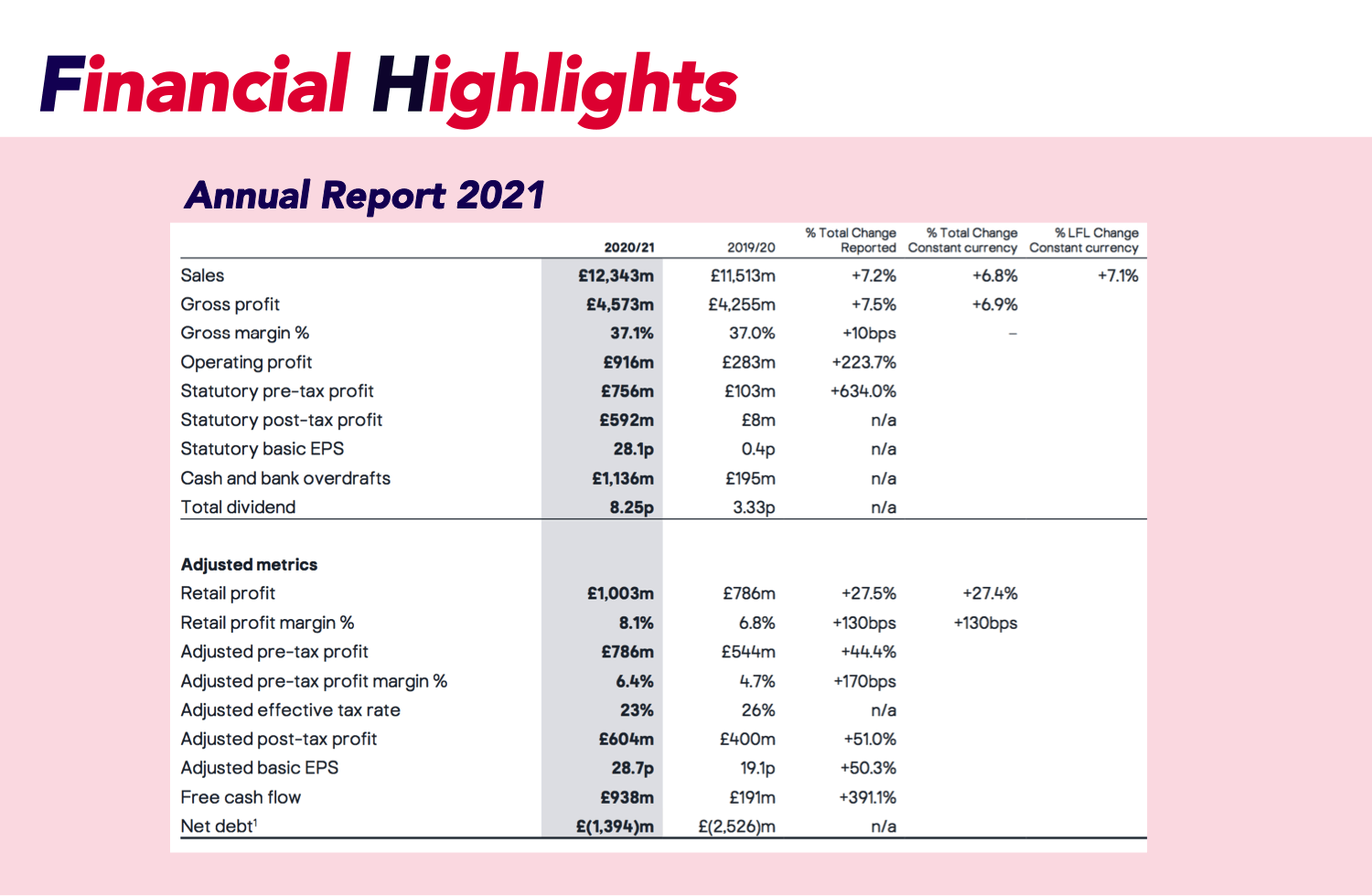

were designated as ‘retailers of essential products’, and therefore could remain open at a time when any excuse to leave the house was gladly taken. As a result, Kingfisher had a very profitable set of full year results: - Sales up

6.8%, driven by strong trading from Q2 and reduced disruption.

- Like-for-like (LFL) sales up

7.1%

with growth across all banners in the UK & Ireland, France, Poland, Romania and Portugal.

- LFL sales up

15.5%

in Q4 20/21 with growth across all retail banners and categories.

- E-commerce sales up

158%; now

18%

of total Group sales (compared with 8% in 19/20).

- Click & collect sales up

226%;

78%

of Group e-commerce sales (19/20:

62%).

- Retail profit up

27.4%, largely driven by B&Q performance.

- Adjusted pre-tax profit up

44.4%.

- Free cash flow of

£938 million, up

£747 million, reflecting higher operating profit, working capital inflow of

£376 million

and

lower capital expenditure

(capex).

As you may have seen in our previous month's top 10 list,

Kingfisher

has been on our radar since releasing their results in April. However, we have had some

reservations

about investing for a couple of reasons. Firstly, when things go back to normal, are we going to see a corresponding

retraction

in these financials? Secondly, to what extent is

Brexit

going to play a part in this company, whose income is somewhat

dependant

on income from the

EU

and for whom

import tariffs could take a sizeable chunk out of the bottom line?

Following what was a fantastic set of annual results for 2020, Kingfisher released some pretty

stellar

results for the

first quarter of 2021

as well, and with them a

cautiously optimistic year-on-year outlook for the rest of 2021 and beyond. As a result, our fears have been somewhat waylaid. Lastly, their annual report also assured investors that the impact of

Brexit

so far has been

cost neutral.

- Sales up 6.8%, driven by strong trading from Q2 and reduced disruption.

- Like-for-like (LFL) sales up 7.1% with growth across all banners in the UK & Ireland, France, Poland, Romania and Portugal.

- LFL sales up 15.5% in Q4 20/21 with growth across all retail banners and categories.

- E-commerce sales up 158%; now 18% of total Group sales (compared with 8% in 19/20).

- Click & collect sales up 226%; 78% of Group e-commerce sales (19/20: 62%).

- Retail profit up 27.4%, largely driven by B&Q performance.

- Adjusted pre-tax profit up 44.4%.

- Free cash flow of £938 million, up £747 million, reflecting higher operating profit, working capital inflow of £376 million and lower capital expenditure (capex).

Images courtesy of Kingfisher PLC.

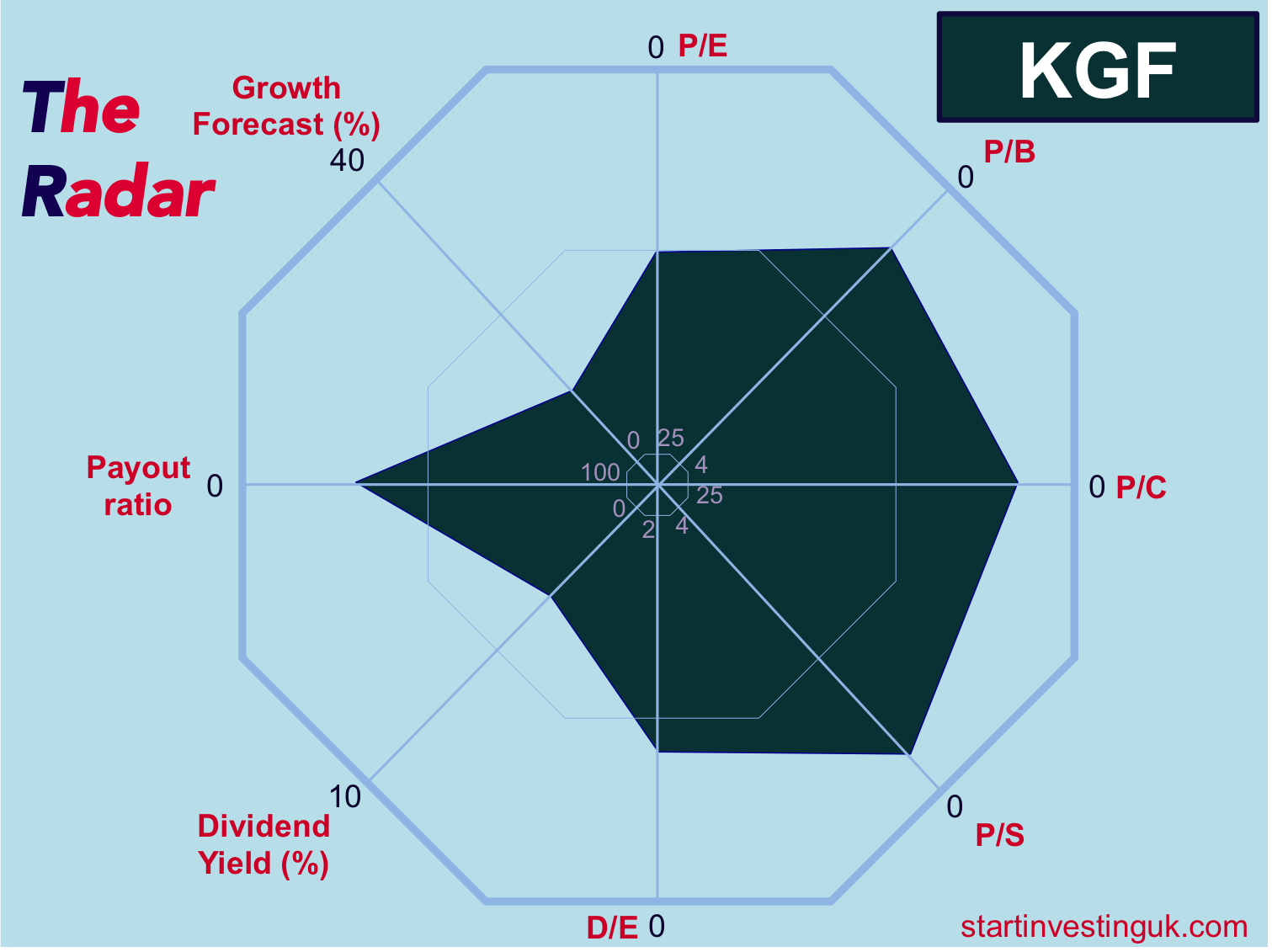

So is Kingfisher PLC

undervalued?

Kingfisher does not score

quite as highly on our metrics as some of our previous

CC picks. The IVI score of

86% is decent but not indicative of being

drastically undervalued, and with a p/e ratio of almost

13, we probably wouldn't put this company alongside some of the others we have invested in so far in terms of pure value. What did strike us about this company though is the

strategic detail

and

insight that is apparent throughout the annual report. They have made

enormous adaptations in a short time to ensure they are

equipped to handle the ongoing challenges of the pandemic and Brexit. We have been

impressed

by the way Kingfisher have

taken advantage of a favourable situation, far from resting on their success, they have pivoted the business to support the changing needs of their customer base. They have even given this project a name, ‘Powered by Kingfisher’, and the payoff now seems to be filtering through to 2021. Their excellent performance so far being down to

4 key initiatives under this banner:

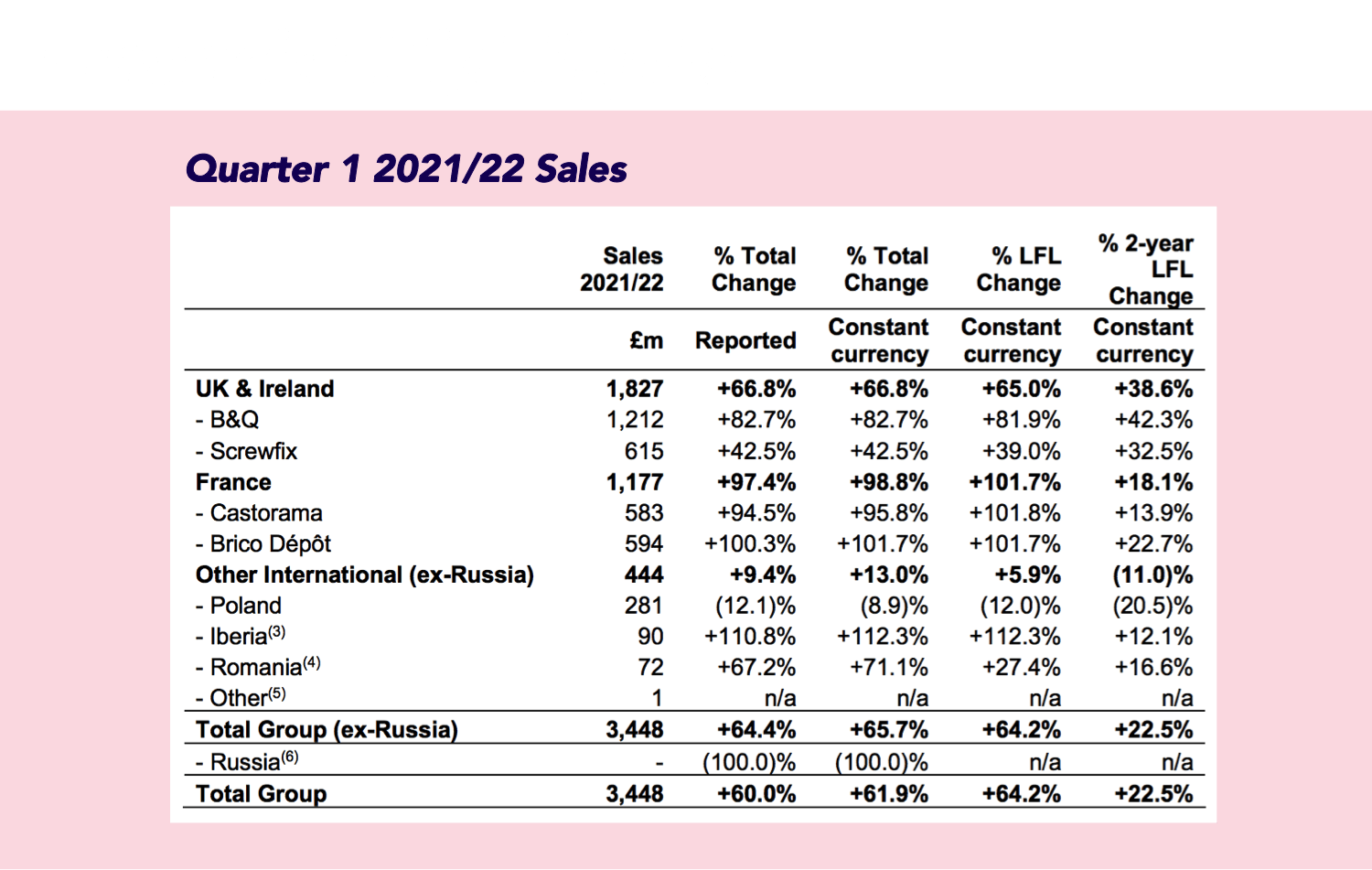

- E-commerce: with online retail now being their fastest-growing channel (2-year growth of over

250%

and accounting for

21%

of total sales), during Q1 Kingfisher established a new agile operating model for their technology and digital teams, and strengthened staff numbers.

- The launch of

Screwfix as an online only retailer in France in late April.

- The launch of their

own brand kitchen range.

- The development of multiple innovative propositions for customers, such as

compact store tests, a new

mobile app

for Screwfix,

self-checkout terminals

and a

new tool for 3D kitchen and bathroom design.

Kingfisher have also reinstated their

progressive dividend policy, meaning they will be paying an

interim dividend for all those who hold the stock before the

3rd of June - a nice bonus! Remember, this means that on the 3rd of June (the ex-dividend date) the share price will

decrease by the amount of dividends to be paid due to market regulation, so we won't be concerned when the price is down a couple of % on that day.

- E-commerce: with online retail now being their fastest-growing channel (2-year growth of over 250% and accounting for 21% of total sales), during Q1 Kingfisher established a new agile operating model for their technology and digital teams, and strengthened staff numbers.

- The launch of Screwfix as an online only retailer in France in late April.

- The launch of their own brand kitchen range.

- The development of multiple innovative propositions for customers, such as compact store tests, a new mobile app for Screwfix, self-checkout terminals and a new tool for 3D kitchen and bathroom design.

- You can read the company's latest

interim report here:

https://www.kingfisher.com/content/dam/kingfisher/Corporate/Images/Other/2021/20210520%202021_22_Q1%20trading%20update_RNS.pdf

- Thierry Garnier, Chief Executive Officer, had this to say about the Q1 results:

“With the strong start to the year, we now anticipate first half sales and adjusted pre-tax profit to be ahead of our previous expectations. Whilst the second half of the financial year remains naturally uncertain, we continue to see supportive long-term trends for our industry and are confident of continued outperformance of our wider markets.”

- You can read the company's latest interim report here: https://www.kingfisher.com/content/dam/kingfisher/Corporate/Images/Other/2021/20210520%202021_22_Q1%20trading%20update_RNS.pdf

- Thierry Garnier, Chief Executive Officer, had this to say about the Q1 results: