Serco: Strong half-year results for the company providing a service that the world needs right now

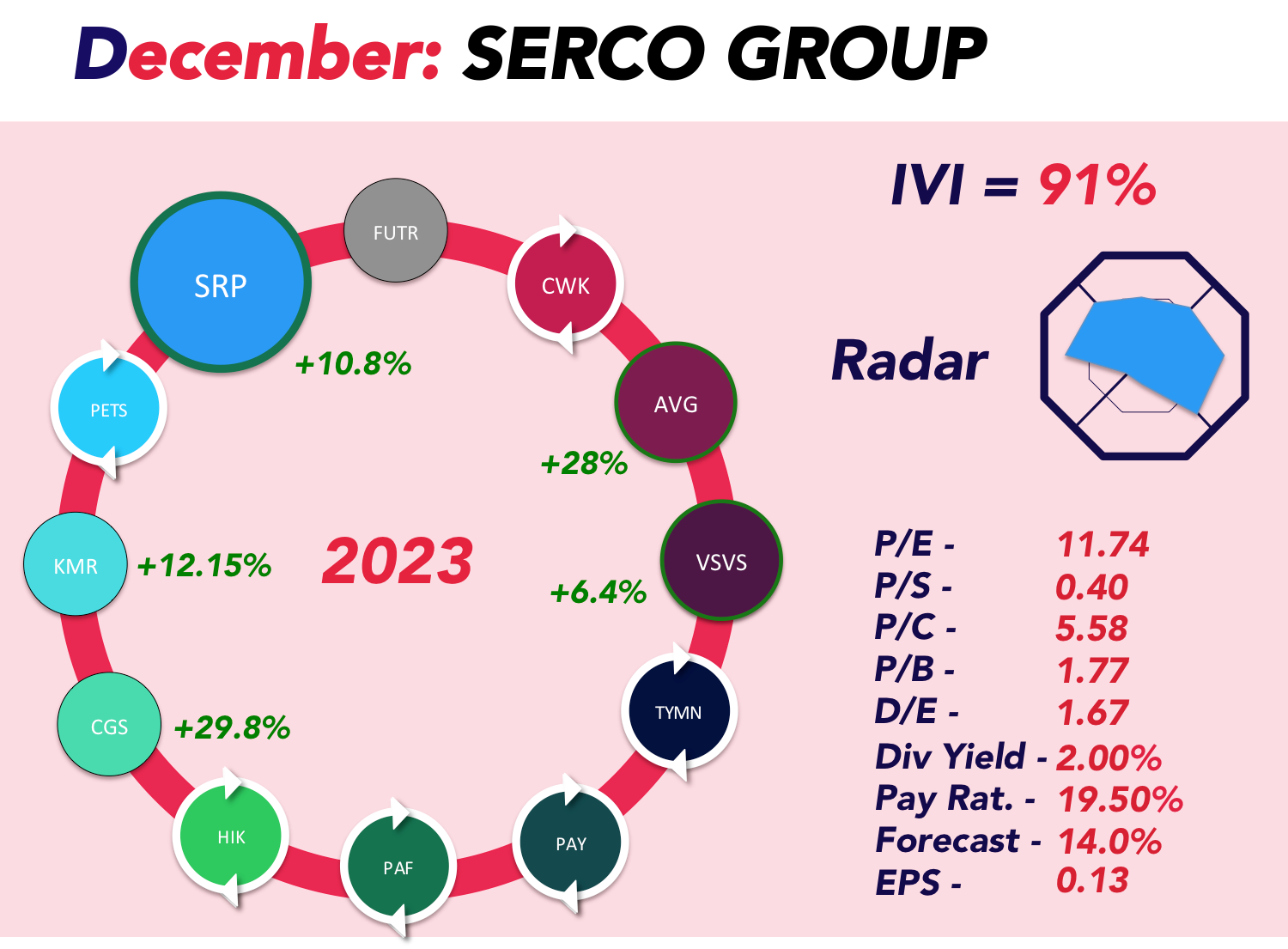

Serco Group (LSE: SRP) has caught our attention with an undervaluation on our metrics despite a 10.5% surge in share price this November, signaling promising momentum . As we delve into whether now is the opportune moment to invest in this FTSE250 company, let's give a brief overview of what Serco is all about.

Serco Group generates revenue through a diverse range of services across various sectors. The company is involved in providing public services to governments globally, and its revenue streams are derived from contracts and projects in areas such as defense, justice, transportation, healthcare, and citizen services.

Here are some key aspects of Serco Group's business activities:

Defence: Serco provides base and operational support engineering, management and information services, as well as nuclear, space, and maritime services for the defense sector.

Justice: The company offers custodial services, asylum seeker accommodation, immigration detention, and detainee transport and monitoring services for the justice and immigration sectors.

Transportation: Serco is involved in rail, ferry, and cycle operations, road traffic management, and air traffic control services for the transportation sector.

Healthcare: The company provides integrated facilities management, clinical and non-clinical support, and patient administration and contact services for the health sector.

Citizens: Serco delivers contact centers, case management, middle and back-office services, and employment and skills services for citizens.

Strategic Acquisitions: Serco strategically acquires businesses to expand its capabilities and market presence. For example, the acquisition of ORS in September 2022 allowed Serco to enter the European immigration services market.

Contracting and Outsourcing: The core of Serco's business model involves contracting with governments to provide essential services that may be more efficiently managed by external specialists.

Immigration services

One area that is particularly interesting in the current global climate is their involvement with immigration. In the context of immigration services, Serco provides a range of solutions to governments, aiding in the management and processing of immigration-related functions.

Detention Centers: Serco operates and manages detention centers where individuals may be held pending immigration hearings or deportation. These facilities provide accommodation and support services, contributing to the company's revenue.

Border Control: Serco may be involved in border control services, assisting governments in managing and securing their borders. This could include technology implementation, personnel training, and infrastructure development.

Asylum Seeker Accommodation: The company offers accommodation services for asylum seekers, ensuring they have housing and support while their immigration status is processed.

Detainee Transport and Monitoring: Serco may be responsible for the transport of detainees between facilities or monitoring individuals subject to immigration restrictions.

Immigration Services Management: Serco's role often extends to the overall management of immigration services, including case management, administrative support, and technology solutions to streamline processes.

Half year results and outlook

Analysts agree with the potential of Serco Group, with five out of six City analysts giving it a 'strong buy' rating and an average price target of 206p (according to

Fool UK), a 30% increase from the current 158p share price, the outlook is buoyant.

In a robust

H1 performance, Serco reported a 13% YoY revenue growth to £2.5bn and a remarkable 52% surge in operating profit to £187.7m, despite challenges in the Asia Pacific and pandemic-related setbacks. The company's strategic entry into the European immigration services market through the acquisition of ORS in September 2022 has exceeded expectations, fostering a strong demand backdrop due to global migration patterns.

As of June, the order book stands at an impressive £14.1bn, setting the stage for a full-year revenue expectation of at least £4.8bn, a 6% increase from the previous year.

The current global migration trend, with a record 108.4 million people displaced by war and persecution in 2023, offers a compelling narrative for Serco. Governments grappling with the surge in migration may continue to outsource services, providing Serco with a stable platform for sustained international growth.

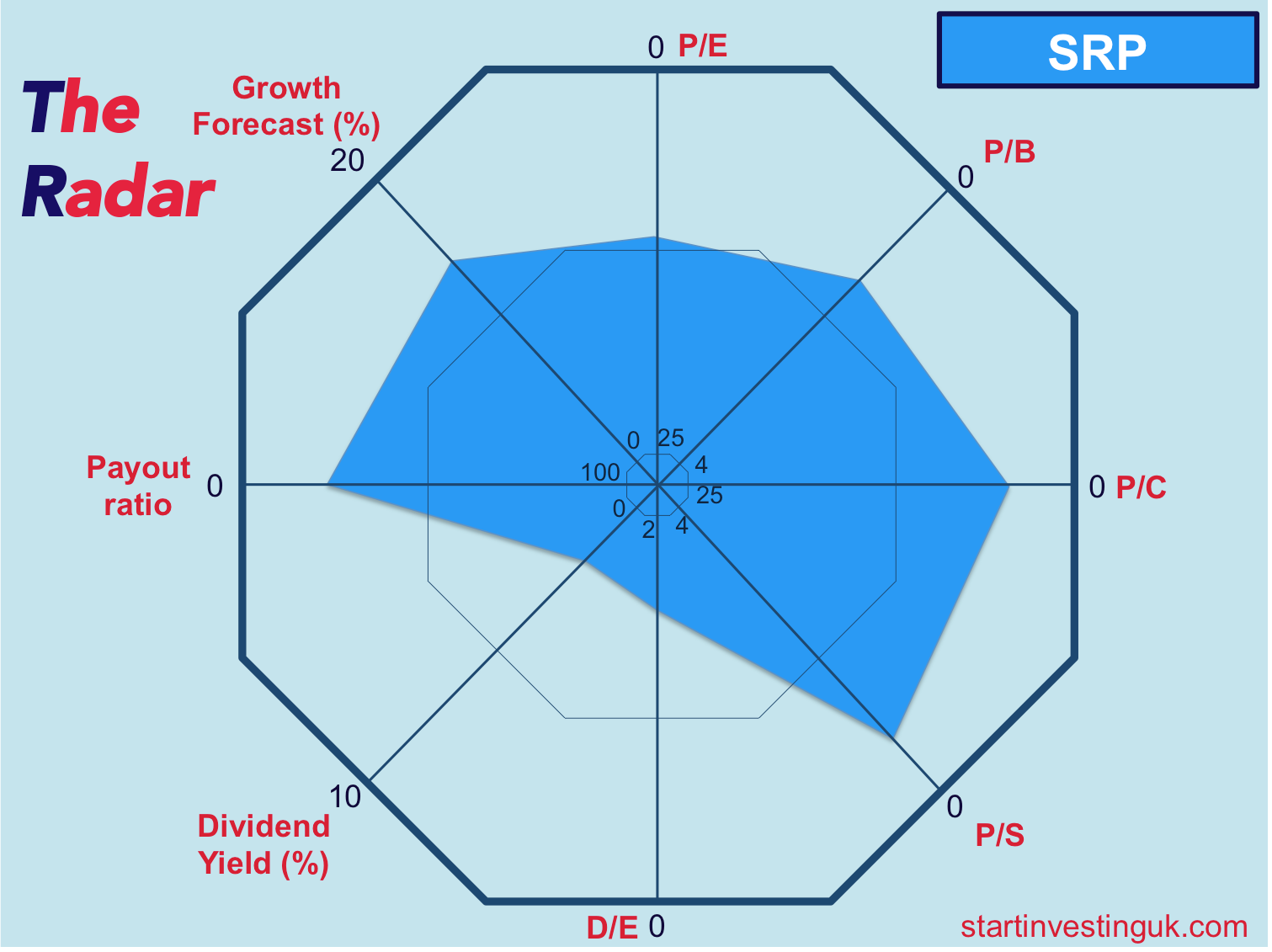

Despite the allure of geographic and sectoral diversity, Serco faces potential challenges, especially in controversial areas such as detention centers. This inherent risk, reflected in a modest forward P/E multiple of 10.6, underscores the company's undervalued status.

With a growing dividend yield of 1.9%, Serco's potential for long-term growth in international markets and its diversified contract portfolio, including major deals with the Australian Department of Home Affairs and the UK Ministry of Justice, position it as a tempting investment prospect.

Here are some key aspects of Serco Group's business activities:

One area that is particularly interesting in the current global climate is their involvement with immigration. In the context of immigration services, Serco provides a range of solutions to governments, aiding in the management and processing of immigration-related functions.

With a growing dividend yield of 1.9%, Serco's potential for long-term growth in international markets and its diversified contract portfolio, including major deals with the Australian Department of Home Affairs and the UK Ministry of Justice, position it as a tempting investment prospect.