Rationale Pets at Home has

benefitted from the pandemic 'pet boom' where pet ownership in the UK increased from

41% (2020) to around 62% (2022).

The company has been

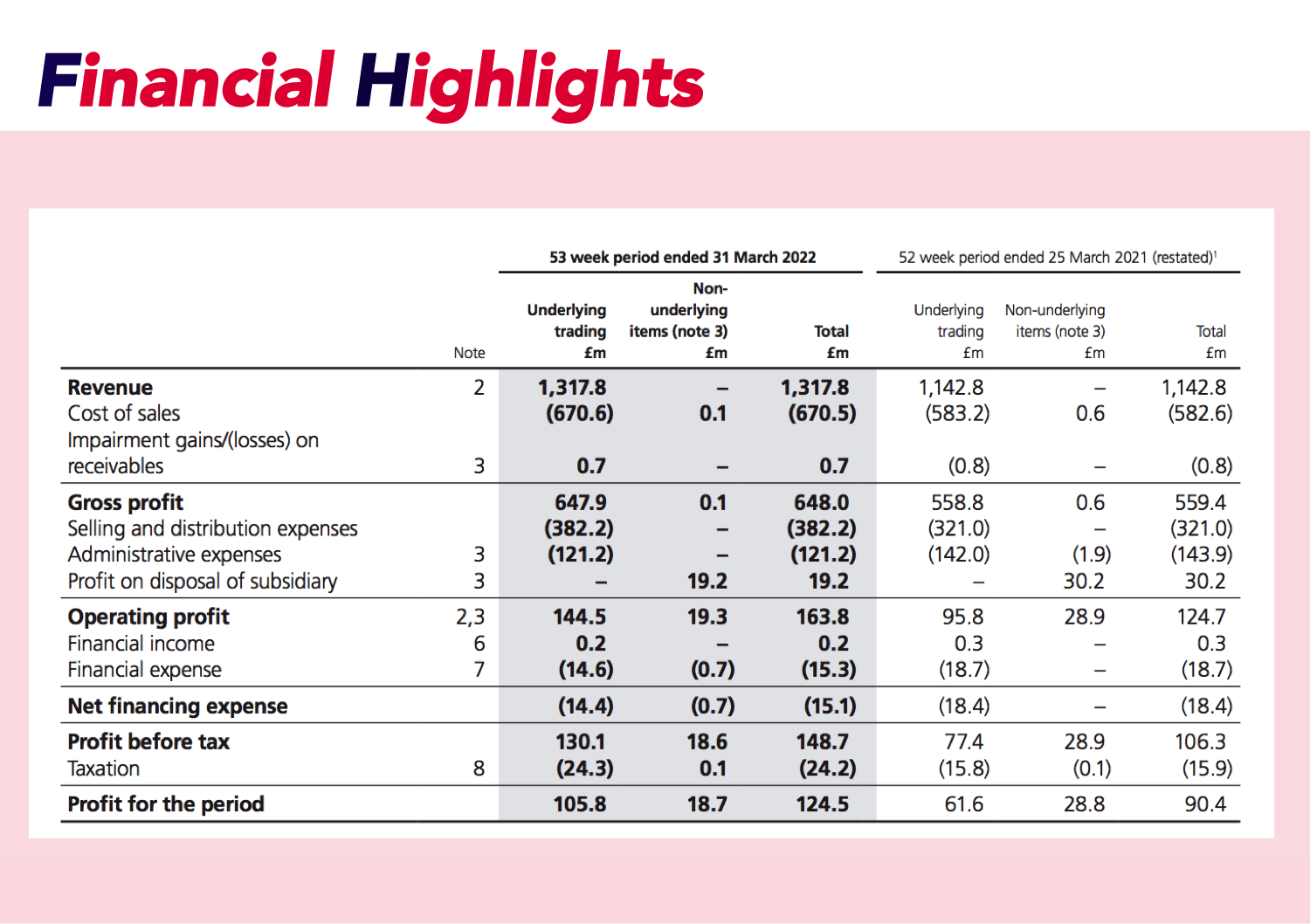

firing on all cylinders in the last 12 months. In May, Pets at Home reported full year revenue of

£1.3bn, showing a rise of

15.8% from the year before. That reflects market share gains across all business areas and record numbers of new customers. Underlying pre-tax profit was ahead of expectations at

£144.7m, up 65.3% year-on-year.

A generous final dividend of

7.5p was announced, up

36% on last year, taking the total annual dividend to

11.8p for the year. The group also intends to launch a 12-month share buyback programme of up to

£50m.

Some analysts are predicting that the boom is now over for PAH, and with inflation combined with a

cost-of-living

crisis nipping at its ankles, there is certainly an argument to be made.

However, pet care has been fairly

recession-proof

in the past, fund manager Terry Smith once jested that pet-owners “would stop feeding their children before they stop feeding their pets,” and if he’s right then Pets at Home could have enough

resilience to keep its stellar run going.

Despite the continued rise of online competitors, PAH's like-for-like retail sales continue to be

very strong. Add to that the group's sterling effort on cost controls, allowing revenue growth to

outpace rising costs, there's a good foundation for future

profit growth.

Vet clinics and grooming rooms provide

extra

revenue streams and also encourage cross-selling in the core retail business, one of the company's biggest

unique selling points.

What about more recent results?Just last week, PAH published their

Q1 results for 2023Top-line highlights include: - Total Group revenue up

7.1% to

£404.7m, with like-for-like revenue up

6.0%, reflecting broad-based growth throughout the quarter.

- Retail revenue increased by

6.6%, and like-for-like revenue up

5.6%.

- All channels remain in growth, with Store like-for-like revenue of

4.3% and Omnichannel like-for-like revenue of

13.5%.

- Vet Group revenue increased by

11.2%, with like-for-like revenue up

8.6%.

- Like-for-like customer sales across all first opinion practices up

4.6% and like-for-like Joint Venture fee income up

9.6%.

What about the share price? Despite a wonderful period for PAH, the share price is down around

30% from this time last year. The market obviously believes the pet boom is coming to its end.

However, we see a group with an enviable client base, with

7.3m ''VIP'' members, and

increasing Puppy and Kitten Club membership. These will help PAH hone their proposition, driving higher sales. But crucially, they're also boosting the number of customers who buy both a product and a service from the group - a leap which massively

increases the average annual spend of these customers and should make them stickier. Pets at Home has only just started to crack this nut, so there's significant potential here.

UK pet ownership continues to look

robust, when a

severe slowdown had been feared after the lockdown-induced tidal wave of new puppies and kittens. It seems

flexible working, and perhaps the renewed

popularity of

rural living, have culminated in the trend having more room for pets than initially thought. That may have a positive effect on demand for a while to come. What's more, a demand shift to more

premium products

and accessories seems to be occurring, possibly due to 'pet humanisation', which is

boosting margins.

PAH has also invested

heavily in its online offering and continues to

ramp up its digital capacity, allowing customers to access all products and services in

one place.

- Total Group revenue up 7.1% to £404.7m, with like-for-like revenue up 6.0%, reflecting broad-based growth throughout the quarter.

- Retail revenue increased by 6.6%, and like-for-like revenue up 5.6%.

- All channels remain in growth, with Store like-for-like revenue of 4.3% and Omnichannel like-for-like revenue of 13.5%.

- Vet Group revenue increased by 11.2%, with like-for-like revenue up 8.6%.

- Like-for-like customer sales across all first opinion practices up 4.6% and like-for-like Joint Venture fee income up 9.6%.