International Personal Finance PLC: A Strong Case for Reinvestment

International Personal Finance PLC (LSE: IPF) is a leading provider of unsecured consumer credit, with operations across nine markets. The company’s commitment to financial inclusion and its robust financial performance make it an excellent candidate for reinvestment this month.

The Case for International Personal Finance

1. Strong Financial Performance

IPF delivered impressive results in its Q3 2024 trading update:

- Customer lending grew by 7% year-on-year (excluding Poland, at constant exchange rates), reflecting strong demand for the company’s products.

- Receivables increased by 11% year-on-year, a key indicator of business growth.

- The annualized impairment rate improved by 2.8 percentage points to 9.2%, showcasing excellent credit quality and repayment performance.

- The company’s guidance for full-year profit before taxation remains strong, projected between £78 million and £82 million, excluding exceptional items.

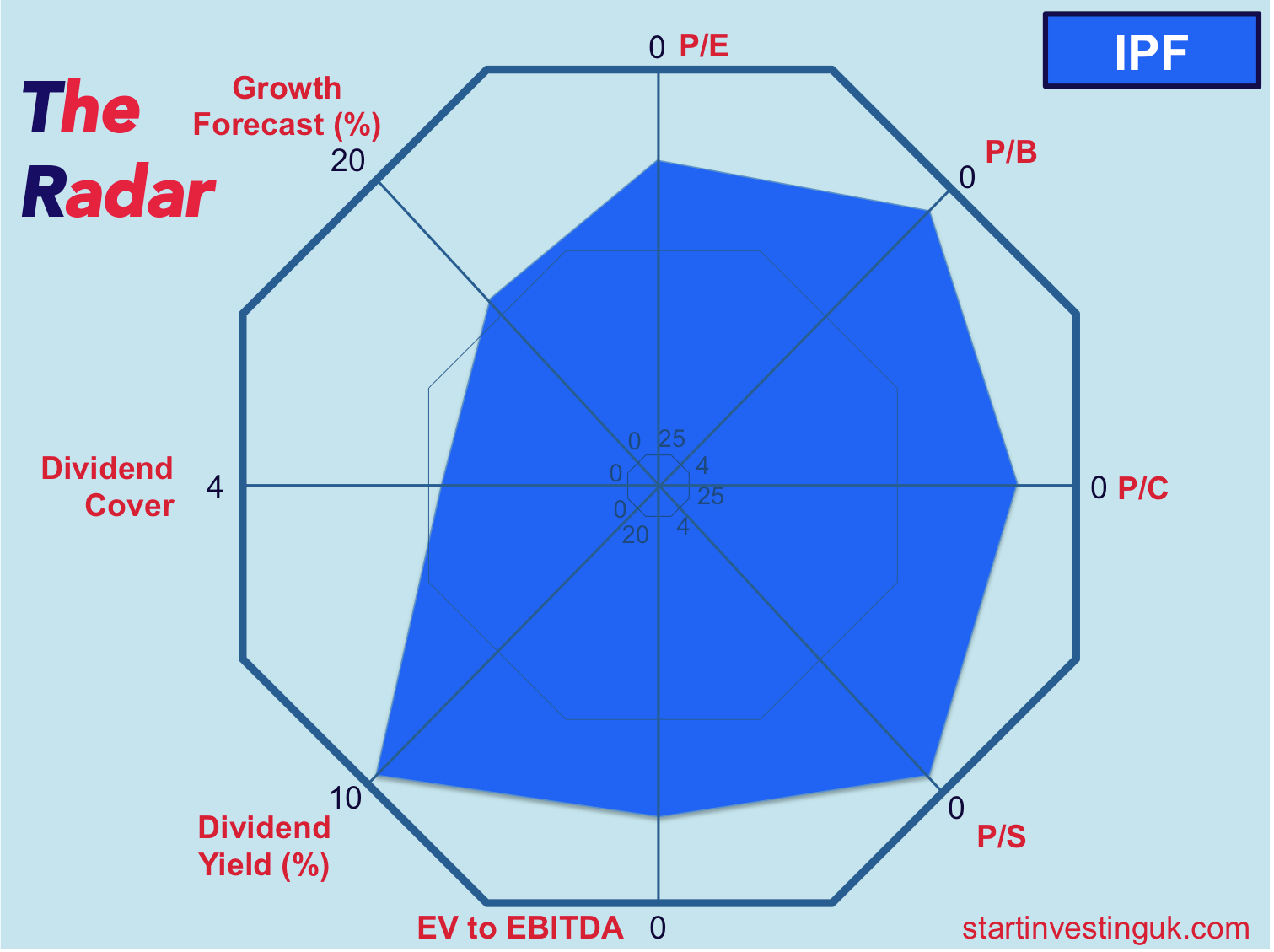

2. Attractive Valuation Metrics

IPF stands out as undervalued compared to industry and market averages:

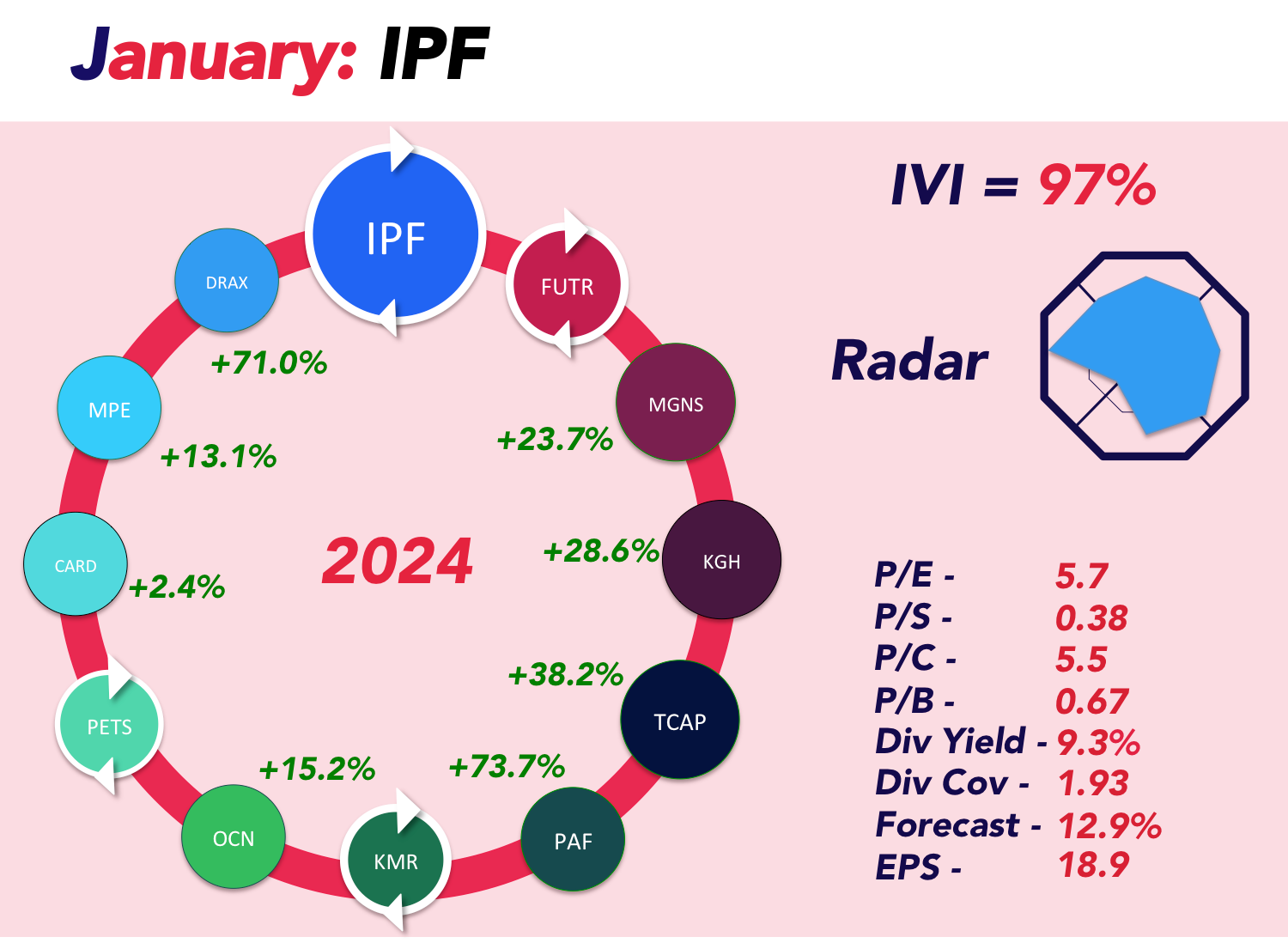

- PE Ratio (f): 5.7, indicating a low price relative to earnings.

- Price to Book Value: 0.59, highlighting the stock’s deep discount to book value.

- Dividend Yield (f): 9.29%, offering substantial income potential for investors.

- PEG Ratio (f): 0.4, reflecting high growth at a low cost.

3. Operational Highlights and Strategic Growth

- The company’s Next Gen strategy focuses on expanding its portfolio of credit and insurance products, further solidifying its market position. Key operational achievements include:

- Successful completion of a £15 million share buyback program, demonstrating confidence in its financial stability.

- Stabilization in the Polish market, with 4% year-on-year lending growth by the end of Q3.

- Equity-to-receivables ratio of 53%, supporting a solid balance sheet.

4. Commitment to Financial Inclusion

- IPF continues to empower underserved consumers through accessible credit solutions. Its mission aligns with global trends toward financial inclusion, offering significant social and economic impact alongside shareholder returns.

Risks to Consider

- While IPF’s performance is robust, investors should monitor a few potential risks:

- Regulatory Changes: The new total cost of credit cap in Romania, effective November 2024, may impact operations, though the company expects this to be immaterial.

- Currency Volatility: Depreciation in currencies like the Mexican peso could affect financial metrics.

- Polish Market Challenges: Although stabilizing, Poland remains a market requiring close attention.

Conclusion

With strong financial performance, an attractive valuation, and a clear strategic direction, International Personal Finance PLC presents a compelling case for reinvestment. Its impressive 9.29% dividend yield and commitment to financial inclusion further bolster its appeal. For investors seeking a high-growth, undervalued opportunity in the financial services sector, IPF looks like a strong pick to kick off 2025.

We will be adding it to our portfolio on Monday.