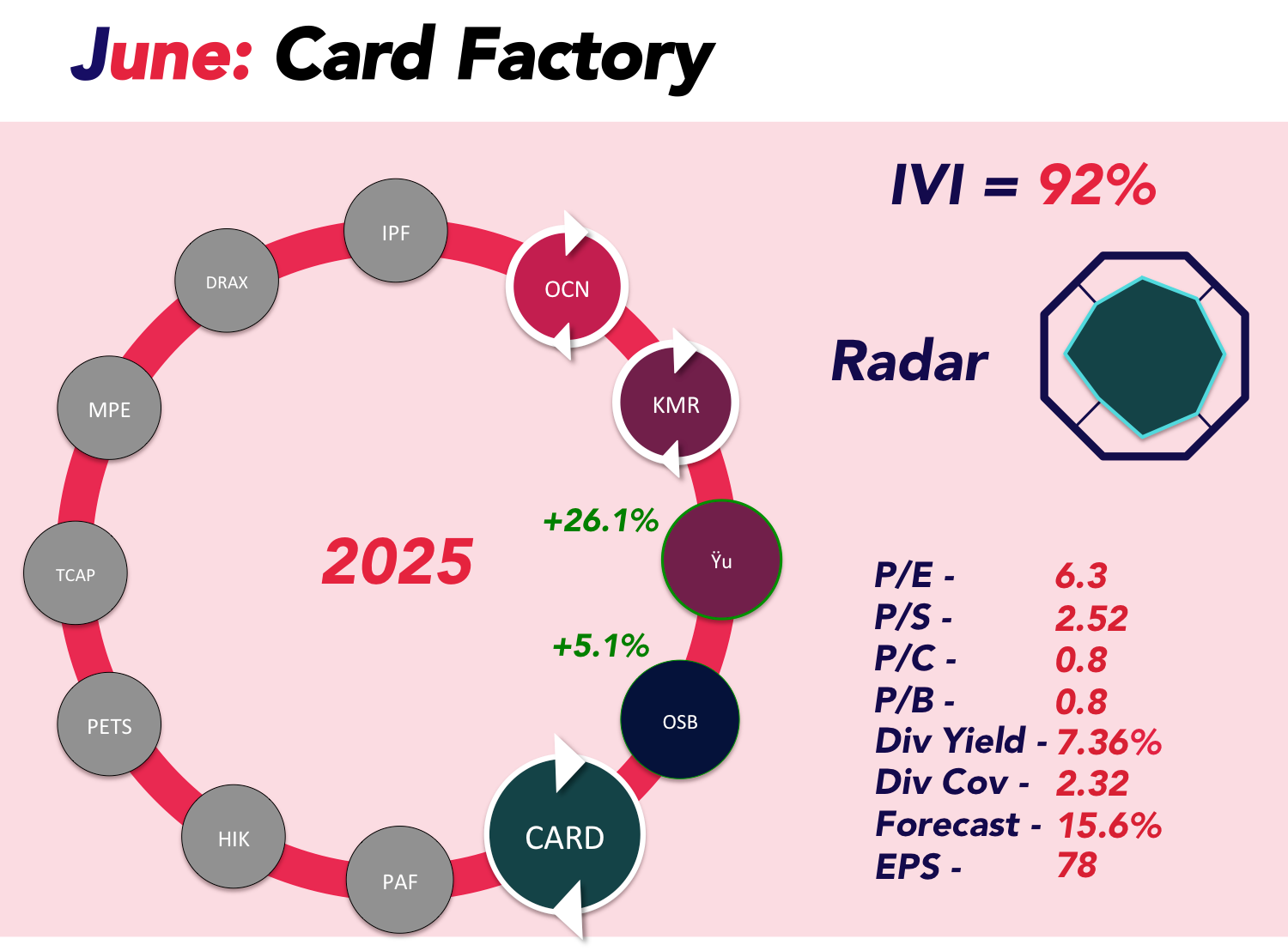

Card Factory PLC: Unwrapping Value in a Resilient Retailer

Card Factory PLC (LSE: CARD), the UK’s leading specialist retailer of greeting cards and celebration essentials, is making a strong case for reinvestment this month. Despite a modest 4% share price dip to 95.5p following its FY25 results, the business continues to outperform expectations and offers an attractive entry point for value-focused investors.

Why We’re Reinvesting in Card Factory

1. Solid Financial Performance in FY25

Card Factory delivered a healthy set of full-year results to 31 January 2025:

- Adjusted profit before tax (PBT) came in at £66m, with actual PBT just slightly lower at £64.1m - underscoring transparent reporting and a disciplined cost base.

- Store like-for-like revenue grew by 3.4%, in addition to the benefit from 32 net new stores and recent acquisitions.

- Total revenue growth outpaced the wider celebrations market, thanks to both organic expansion and new product development.

In an environment where many retailers are delivering gloomy updates, Card Factory is quietly beating the odds.

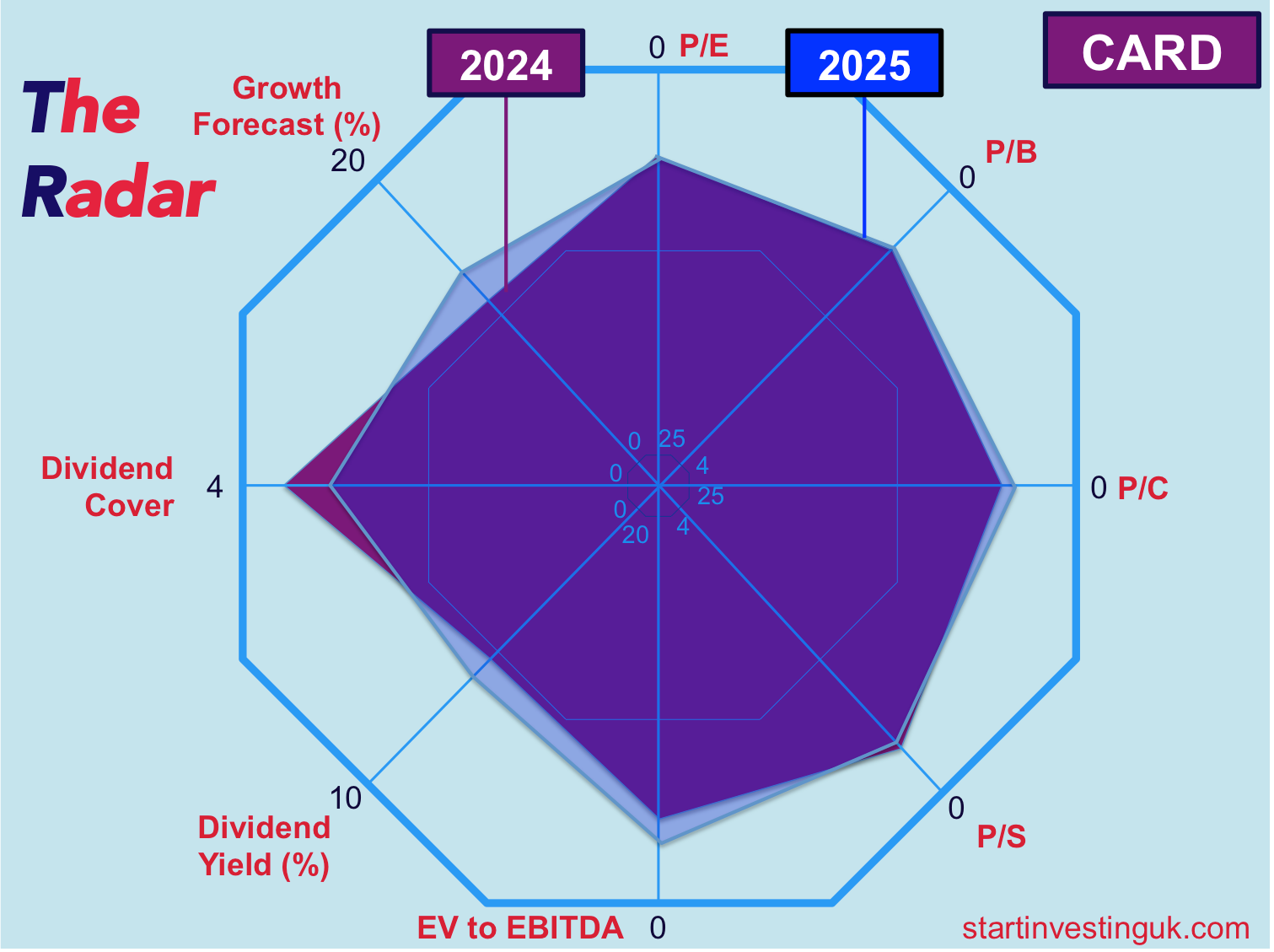

2. Attractive Valuation Metrics

Even after the share price uptick over the last year, CARD still looks inexpensive:

- Forward P/E Ratio of just 6.3x, based on Edison’s updated EPS estimate of 15.2p for FY26.

- Net debt (excluding leases) sits at £58.9m- less than 1x EBITDA - leaving the company in a manageable financial position despite recent acquisition and dividend outflows.

- Leverage, including leases, remains conservative at 1.3x EBITDA.

The market appears to be pricing in a level of risk that doesn't reflect the company’s improving fundamentals.

3. Clear Outlook and Sensible Guidance

Management isn’t overpromising - guidance for FY26 includes:

- Mid-to-high single-digit Adjusted PBT growth

- Margins in line with FY25

- Mid-single-digit sales growth, annually

Even with higher wage and national insurance costs expected to hit to the tune of £14m, Card Factory plans to offset these pressures through efficiency programmes, product range development, and pricing strategy.

4. Strategic Growth Across Borders

Card Factory is no longer just a UK story:

- Acquisitions in Ireland and the US hint at an ambition to become a global celebrations brand

- Retail partnerships now span the UK, Ireland, Australia, the US, and the Middle East

- Growth is not just about stores, but also wholesale channels and online offerings

That said, we’d prefer the company to retain more of its cash to fuel this international expansion, rather than distributing sizeable dividends.

5. Resilience in a Challenging Retail Landscape

The greeting card industry isn't without risk - highly commoditised products and economic exposure make it vulnerable. Clintons Cards has gone bust twice in the past decade. But Card Factory has so far avoided such pitfalls, proving more resilient than peers with:

- A more efficient cost base

- Greater scale and supply chain leverage

- Clear profitability, even through inflationary headwinds

Risks to Consider

- Consumer Sensitivity: Greeting cards and party products are discretionary, and sales may soften in a downturn.

- Retail Overhead Pressures: Living wage increases and business rates remain ongoing concerns for the sector.

- Balance Sheet: While acceptable, debt levels should be monitored, especially with further international expansion on the horizon.