A company called 'Secure Trust Bank' - what could possibly go wrong?

I mean - come on - the name sounds like something a supervillain would use to store his gold bars, it practically screams “nothing to see here.” But peel back the branding, and there’s actually a fascinating investment case under the surface. One that’s been clouded by litigation, discounted by the market, and - just maybe - starting to turn the corner.

Let’s dive in.

First, the Elephant in the Room: The Car Finance Scandal

You may know that the UK financial world has been dealing with a new wave of litigation - this time about car finance.

At the heart of the issue is whether car dealers had a fiduciary duty to disclose commissions when arranging loans for customers. The Court of Appeal said they did (which surprised just about everyone), and the case is now headed to the Supreme Court later this summer. Depending on the ruling, banks and lenders could be on the hook for billions in redress.

Secure Trust is one of the names caught up in this mess - though it's important to note, their exposure is relatively limited. While giants like Lloyds, Santander, and Close Brothers have big motor finance divisions, STB’s involvement is far more modest. They’ve already taken early provisions, sold off some of the defaulted loan book, and are actively managing the risk.

Still, when panic sets in, it doesn’t discriminate. STB’s share price was punished along with everyone else.

So, Why Has the Share Price Been Clobbered?

Litigation fears, plain and simple. Even though the redress scheme hasn't been finalised, and STB is on the lower end of industry exposure, the market ran for the hills. But now… sentiment is shifting.

Just recently, STB’s stock jumped 33% in a single day on news that the Treasury is stepping in—urging the courts to ensure any redress scheme is proportionate and sensible. Translation? The nightmare scenarios are looking less likely, and investors are beginning to reprice the stock accordingly.

Under the Hood: Fundamentals Are Seriously Strong

Here’s where it gets interesting. STB isn’t just “cheap.” It’s absurdly cheap.

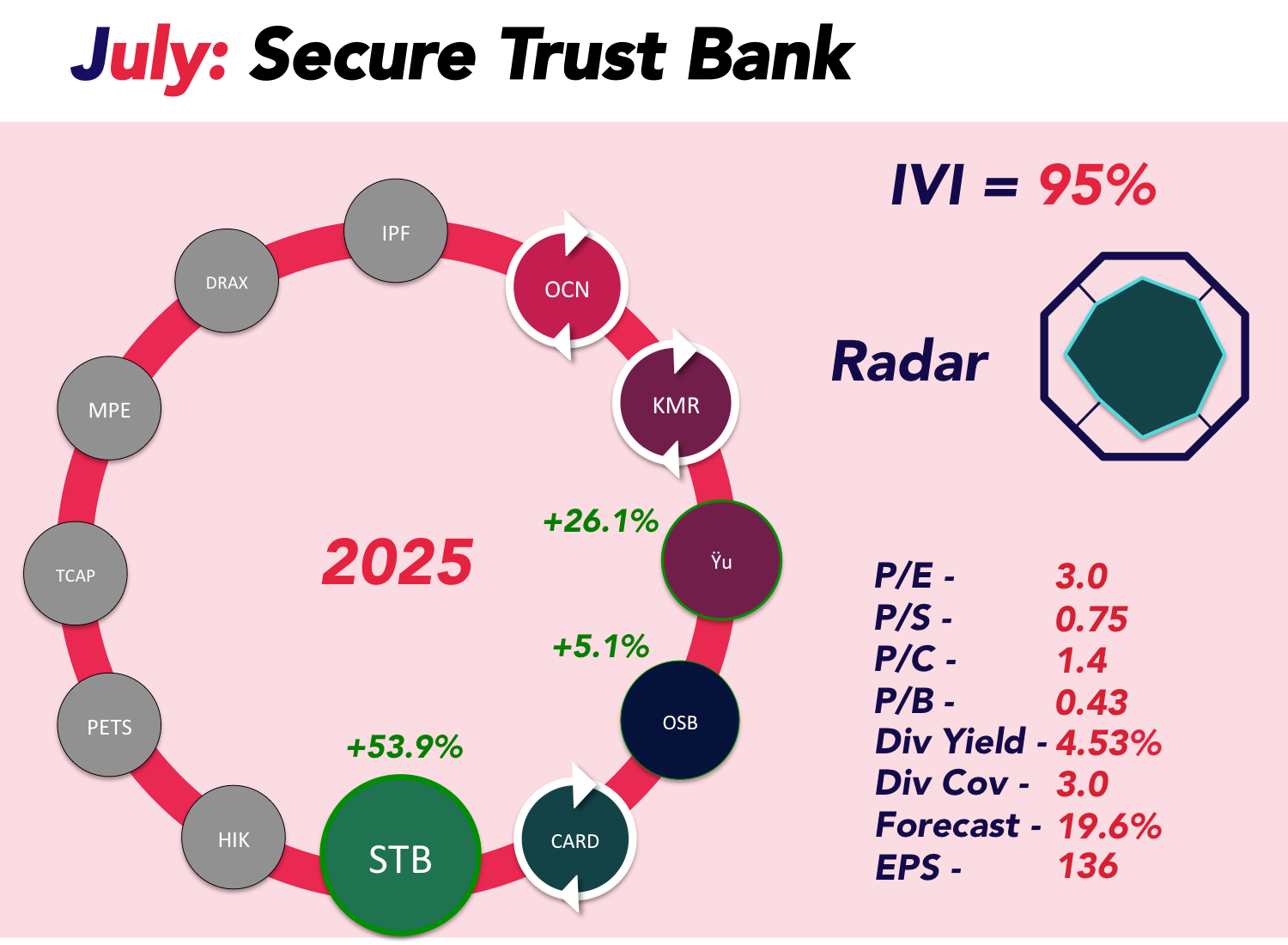

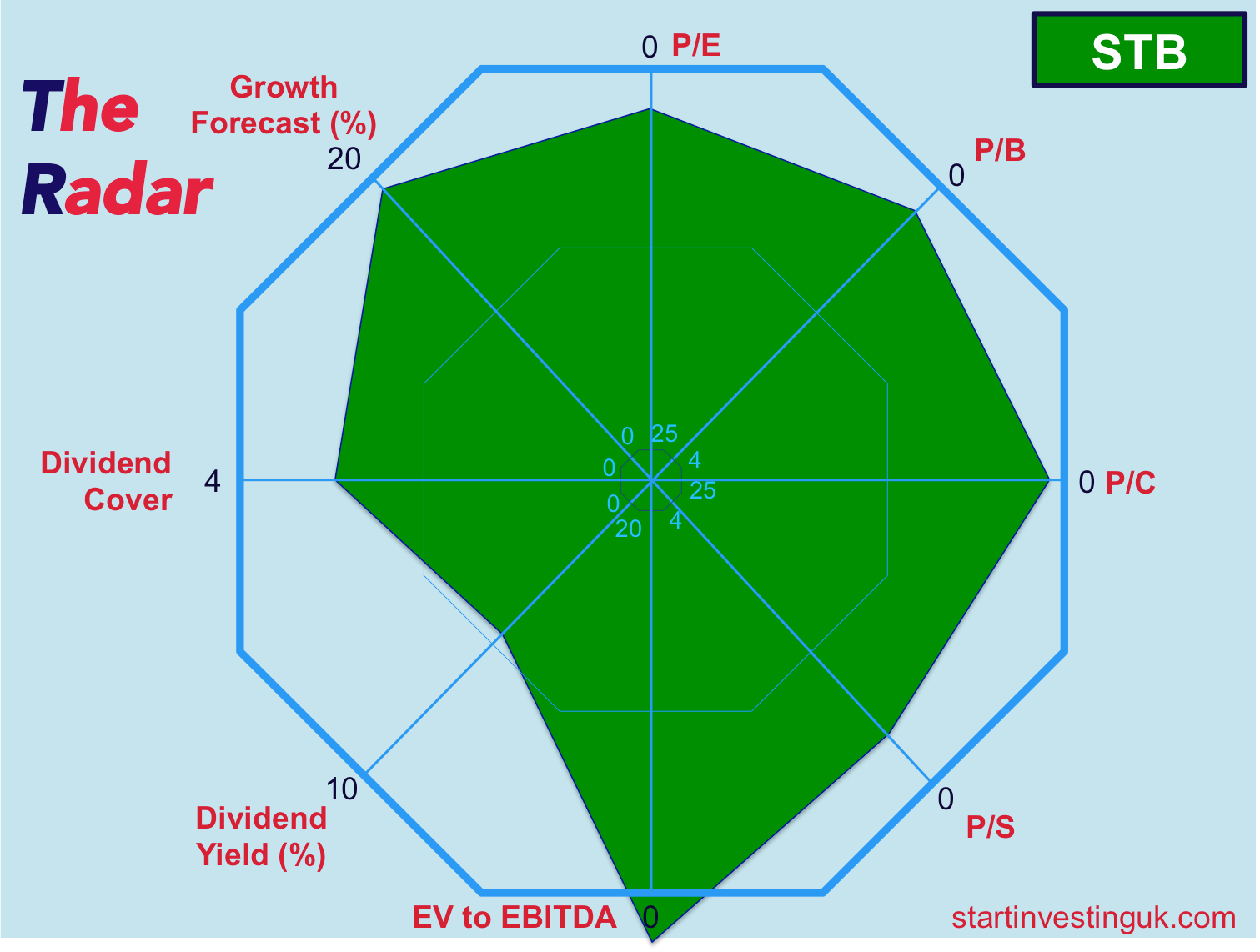

Check out the valuation stats at the top of this page. Basically, you're buying a fast-growing, cash-generative bank for less than half its book value, and getting paid a solid dividend while you wait.

Even the EV/EBITDA ratio is negative, which can happen when the enterprise value is deeply discounted vs earnings—another sign of extreme undervaluation.

And the business performance? Still strong.

- Net lending grew 10.5% YoY and is approaching their £4bn target.

- Deposits up 15.4% YoY, showing customer confidence.

- Cost savings on track with £8m in efficiencies from Project Fusion.

- Management just completed a £25.8m sale of defaulted loans,

freeing up resources to focus on early-stage arrears.

CEO David McCreadie is, to paraphrase, “confident.”

What’s the Market Missing?

In our opinion: risk asymmetry.

The legal case is serious, no doubt. But as sentiment shifts - thanks to a likely proportionate outcome and government involvement - the market may be realising it overcorrected. Secure Trust has limited exposure, is well provisioned, and is still growing. Yet it's trading like a distressed asset.

We're hoping this is a case of "Buy the rumour, sell the news."

Conclusion: STB Deserves a Closer Look

We believe:

- The Supreme Court won’t throw the whole sector under the bus

- Redress will be proportional, not catastrophic

- STB’s limited exposure gives it a built-in safety buffer

Therefore, here’s what we're getting:

- A growing bank with solid fundamentals

- One of the cheapest valuations in UK finance

- A near 5% dividend while you wait

- Upside potential if/when the litigation dust settles

It’s not without risk - but in investing, sometimes the best opportunities lie where others are too spooked to look. We will be adding STB to our portfolio on Monday morning.