Begbies Traynor Is Booming – And That Might Be a Bad Sign for Everyone Else

When a corporate insolvency firm is reporting its tenth consecutive year of growth, it’s probably not because the economy is in great shape. Begbies Traynor has quietly become one of the most reliable performers in the UK small-cap space, and while that’s good news for shareholders, it’s a little ominous for the wider market. Business is booming – because a lot of other businesses aren’t.

But look past the macro gloom, and you’ll find a company executing a smart, scalable strategy across restructuring, advisory, and property – all while throwing off cash and growing its dividend.

Let’s take a look.

This Isn’t a Turnaround - It’s a Consistent Climb

While investors often look for dramatic turnaround stories or distressed discounts, Begbies Traynor has taken the less flashy route: steadily building scale through a proven strategy of organic growth and bolt-on acquisitions.

And it’s working.

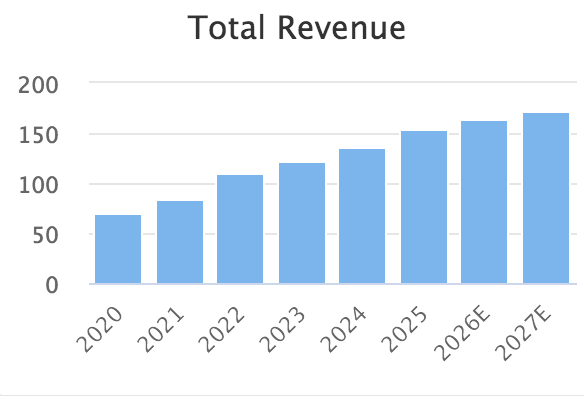

- Revenue up 12% YoY, with 10% of that from organic growth—no one-hit wonders here.

- Adjusted EBITDA up 11%, outpacing revenue growth.

- Free cash flow up 56%, now £19.4m for the year.

- Net cash positive for the first time in years, despite spending £9.4m on acquisitions, £6.3m on dividends, and £1.6m on buybacks.

This is a business that's expanding without overreaching, paying shareholders, and still keeping dry powder for growth.

Begbies Traynor Is Booming – And That Might Be a Bad Sign for Everyone Else

When a corporate insolvency firm is reporting its tenth consecutive year of growth, it’s probably not because the economy is in great shape. Begbies Traynor has quietly become one of the most reliable performers in the UK small-cap space, and while that’s good news for shareholders, it’s a little ominous for the wider market. Business is booming – because a lot of other businesses aren’t.

But look past the macro gloom, and you’ll find a company executing a smart, scalable strategy across restructuring, advisory, and property – all while throwing off cash and growing its dividend.

Let’s take a look.

This Isn’t a Turnaround - It’s a Consistent Climb

While investors often look for dramatic turnaround stories or distressed discounts, Begbies Traynor has taken the less flashy route: steadily building scale through a proven strategy of organic growth and bolt-on acquisitions.

And it’s working.

- Revenue up 12% YoY, with 10% of that from organic growth—no one-hit wonders here.

- Adjusted EBITDA up 11%, outpacing revenue growth.

- Free cash flow up 56%, now £19.4m for the year.

- Net cash positive for the first time in years, despite spending £9.4m on acquisitions, £6.3m on dividends, and £1.6m on buybacks.

This is a business that's expanding without overreaching, paying shareholders, and still keeping dry powder for growth.

Two Pillars, Both Firing

Begbies runs on two main engines: Business Recovery & Advisory and Property Advisory.

- On the restructuring side, they continue to dominate. They’re number one in the UK by volume of insolvency appointments and have been handling larger, more complex cases.

- The advisory arm has tripled in size since 2020, pushing into special situations M&A, funding, and forensics. These are high-margin services that scale well and deepen client relationships.

- Property services, which include everything from valuations to auctions, saw strong growth and are becoming a key contributor—especially as auctions ramp up and demand for property services rebounds post-pandemic.

Management keeps expanding the professional bench with targeted senior hires, which suggests they’re building not just scale, but expertise.

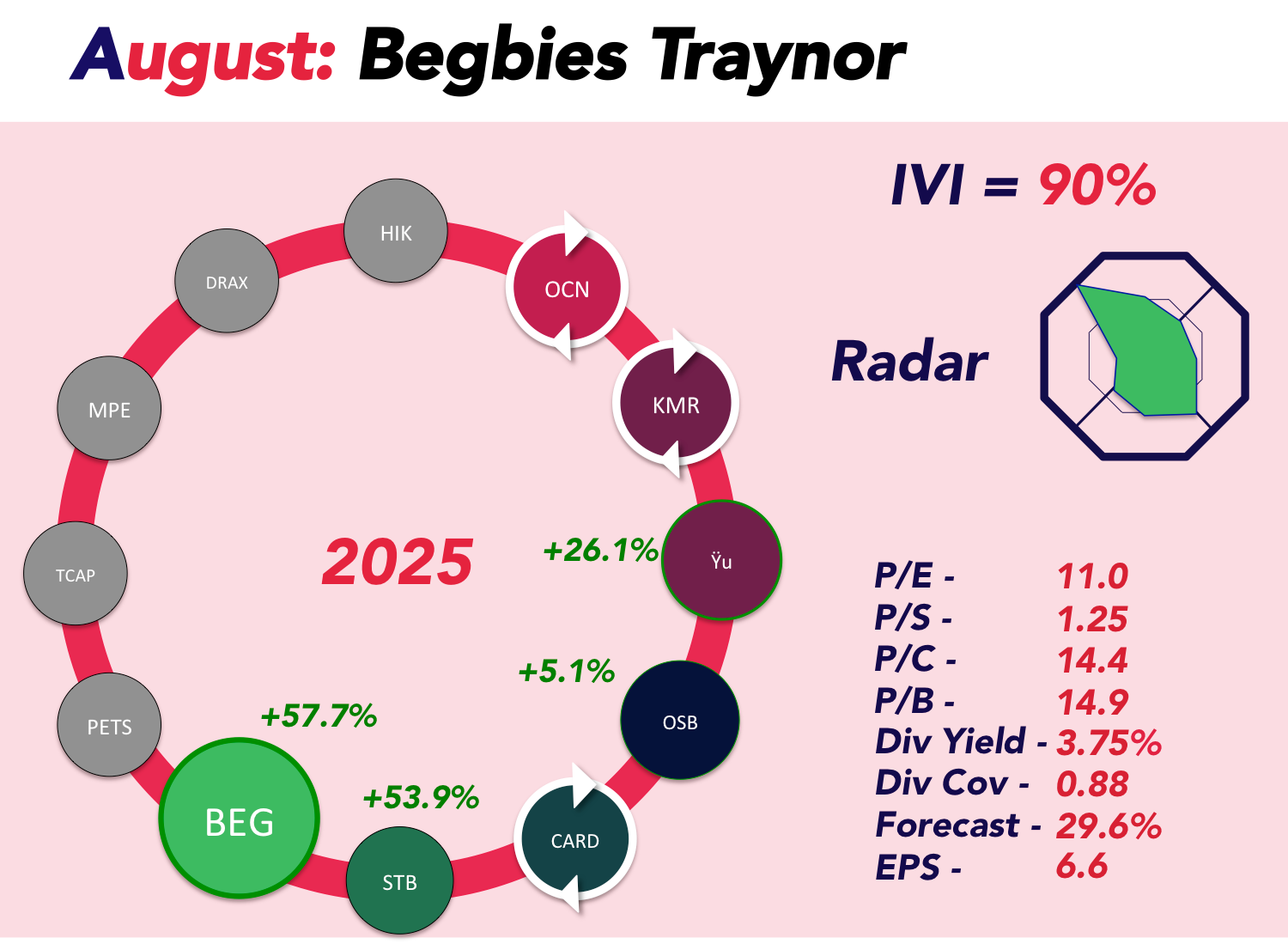

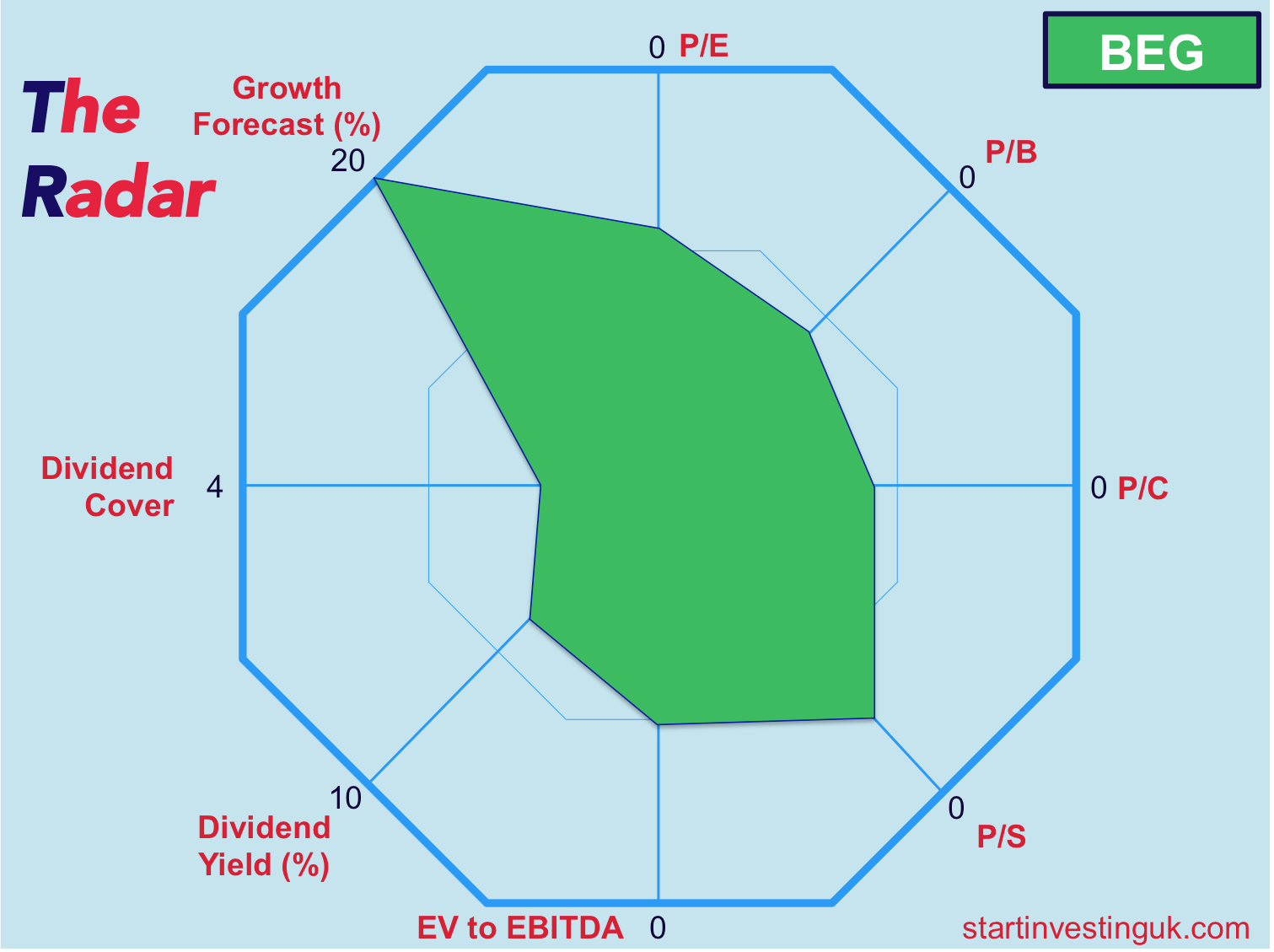

Dividend Growing. Buybacks Coming. Market Still Yawning.

Despite all this, the market has barely looked up.

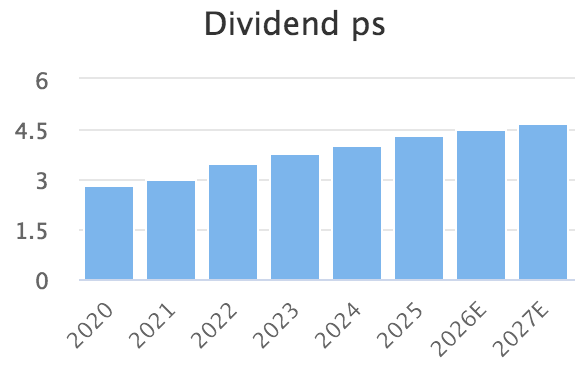

Begbies’ dividend just rose 8% - its eighth year of consecutive increases - and a 1 million share buyback is now in play to offset option dilution. In a higher-rate environment where free cash is king, that should be music to investors’ ears.

Yet it’s still trading at modest multiples and a muted valuation.

Part of that is due to the nature of the business—it’s complex, not easily comparable, and doesn’t scream “growth stock” on the surface. But strip back the labels and you’ll find a highly cash-generative, counter-cyclical firm, perfectly positioned to benefit from ongoing economic uncertainty.

What’s the Market Missing?

- Consistency. Ten years of profitable growth through Brexit, COVID, and inflation cycles is no accident.

- Optionality. With net cash, strong FCF, and committed bank facilities, Begbies can pounce on opportunities others can't touch.

- Counter-cyclicality. Tough markets boost insolvency and restructuring demand. That's not a bug—it's a feature.

- Scalability. Advisory services like forensics and special situations M&A scale with demand, and Begbies is investing in the talent to meet it.

Conclusion: Not Flashy, But Exceptionally Solid

We think Begbies Traynor is a textbook case of a compounder hiding in plain sight.

Here’s what you’re getting:

- A decade-long track record of growth and capital discipline

- Exposure to counter-cyclical revenue streams in restructuring

- A fast-growing advisory and property platform

- A solid dividend (4.3p) with room to grow

- Net cash, healthy FCF, and a strong acquisition pipeline

No, it’s not going to 10x overnight. But as a core holding in a diversified UK equity portfolio? It’s hard to find fault.

We will be adding BEG to our portfolio on Monday morning.